The A2 Milk Company

Every month we'll be sharing a breakdown on our past or present investments. Previously we’ve discussed our investments in Food & Life Companies in Japan and Magna International in Canada. Today we'll discuss our rationale for our investment in The a2 Milk Company in New Zealand.

The A2 Milk Company (NZE: ATM / ASX: A2M)

The A2 Milk Company is known for producing A2 cow milk that is free of A1 beta-casein protein. It also produces infant and toddler milk products sold in Australia, New Zealand, China, the US and the UK. Research has shown that A2 protein is digested differently to A1. The A2 protein has been proven scientifically to cause less digestive issues for people. There are many people who feel uncomfortable after drinking ordinary milk or lactose-free milk, yet they can enjoy A2 Milk without any discomfort.

A recent decline in share price

The stock value of A2 Milk dropped 72% from its 2020 highs, despite being net cash positive. This is due to border closure during the pandemic causing a significant decline of sales volume for infant formula in China and therefore A2 Milk holding a lot of unsold goods.

With its 1.4 billion population, China has been A2 Milk’s focus for years. A2 Milk has been highly reliant on cross-promotion by daigous as they make the brand more popular in through word-of-mouth referrals. Daigous are personal shoppers that often start out as Chinese tourists or international students, and in this case, purchase A2 milk’s infant formula products in New Zealand and Australia, then take the products back to China and resell them with commission. Foreign infant formula brands continue to be the most popular options for Chinese parents who want to ensure they are getting products with proper quality control.

The decline in daigou sales are also partially due to Chinese parents’ preferences to local products with cheaper prices and quicker delivery. It may also be due to the declining birth rate in China and significantly higher wholesale price of A2 Milk products. Despite these short term setbacks, cross-border travel restrictions and on-going inventory de-stocking are likely to be a temporary issue. A2 Milk have started to destroy dated infant formula inventory and have slowed down in sales to help reduce an oversupply of products in the infant formula market.

A potential turn around

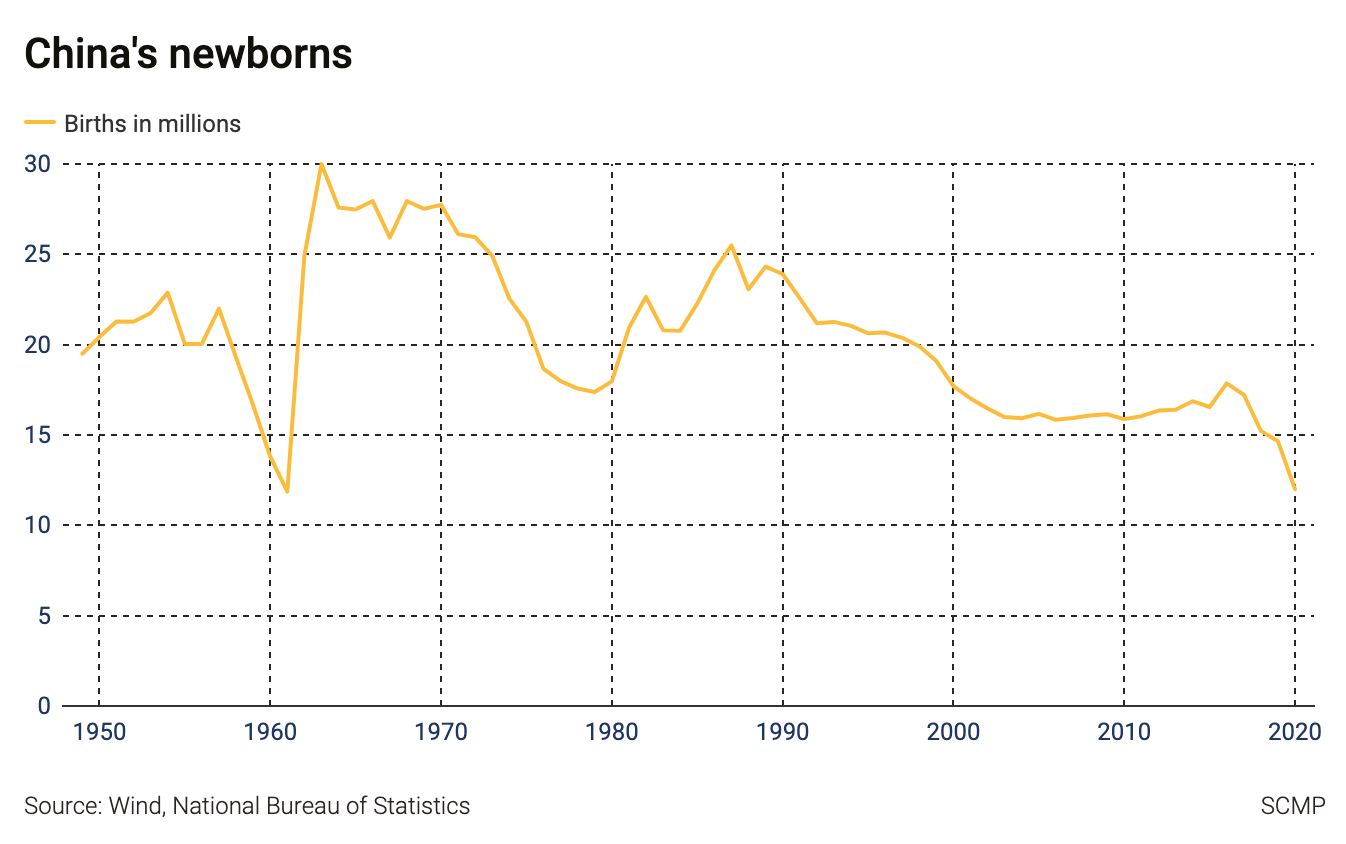

In the recent months the Chinese government have introduced a three-child policy in which each couple would be permitted to have up to three children. This is a major policy shift from the existing limit of two children after recent data showed a dramatic decline of 18% birth rate from 14.65 million births in 2019 to 12 million births in 2020. A report by demographers at Renmin University of China estimated that the policy would probably lead to an annual increase of 200,000 to 300,000 births in the next five years which is a slight increase from the rate of 12 million births last year in 2020. Some families are ready to have a third child. Therefore, A2 Milk is still confident in the long term potential for their infant formula and other opportunities they have in China.

Furthermore, the Chinese government has noted that it would strive to “reduce non-medical abortion” without providing further details. This misuse of abortion as a tool of state policy in China may increase the birthrate.

With my estimated numbers for 2021, we could see a general decline across the board, with net income estimated to be down 37%, revenue down by 21% and gross profit down 29%. This isn't great, but the cross-border travel restrictions and the ongoing inventory de-stocking are likely to be temporary issues. With currently a 66% decrease in stock price from its highs, compared to an average decrease of key numbers (revenue, margins etc.) at 26%, A2 Milk may be a bargain.

A well run company before this pandemic

Before the pandemic, A2 Milk had a P/E ratio of 39. This is high but it is likely because of their great performance before the pandemic:

Earnings per share had consistently gone up (from 0.04 in 2016 to 0.52 in 2020)

Net income as % of revenue was good and was getting higher (from 5% in 2021 to 22% in 2020)

Operating expense as % of gross profit is reasonable at around 45%

Gross margin is improving (from 34% in 2011 to 56% in 2020)

Debt, and therefore interest expense, is non-existent

One thing to note about net income is the projected 2021 would be of 17% of revenue which is still decent

Another thing to note about projected gross margin is that it would be 50.3% in 2021 which is still good and matches their gross margin in 2018. The stock price in 2018 was 11.90 compared to 6.72 today

What isn't great:

There are a few things which are less positive. A number of them are less to do with their balance sheet and more to do with uncertainty of what happens with current affairs:

Number of shares has slowly risen over time

Uncertainty of when China will open its borders

Uncertainty of effectiveness of the China three-child policy

The effect of the three-child policy is still uncertain at the moment. Many young Chinese’s attitudes towards childbirth have changed because they want lives without constant worries of raising a child under a higher cost of living. However, we cannot underestimate the state’s ability to change this course.

In reality, the company's 2021 performance will be similar to their 2018 numbers, when A2 milk had almost double the valuation. Combine this with the fact this issue is likely to be temporary and the company is either at below fair value or undervalued.

Disclosure:

We went long A2 Milk Company (ASX) in June 2021 and have an 11% gain so far, but we have no plans to sell it any time soon.

Disclaimer:

This is not investment advice. Our content to be used for informational purposes only. It is important you do your own analysis before making any investment based on your own personal circumstances.

About:

Sign up to our free newsletter for more analysis & recommendations:

Stay invested and follow Giles Capital on Twitter at @GilesCapital.