Potential value in ASOS plc (LON:ASC)

Every month we'll be sharing a breakdown on our investment ideas. Previously we’ve discussed our investments in The a2 Milk Company in New Zealand and Airtel Africa in the UK. Today we’ll discuss our potential investment in ASOS plc in the UK.

ASOS plc (LON:ASC)

ASOS plc is a British online fashion and cosmetic retailer. The company was founded in 2000 in London and it is primarily aimed at young adults. The stock would have delivered huge returns if one invested in the 2000s, but since then it has been quite volatile.

The stock was brought to my attention by articles written about the investor Nick Sleep. For a good read see Shareholder Letters of Nick Sleep of Nomad Investment written by Daniel Lee.

ASOS may follow what Nick Sleep calls a 'Scale Economics Shared’ model. He says on his theory: “Scale Economics Shared operations are quite different. As the firm grows in size, scale savings are given back to the customer in the form of lower prices. The customer then reciprocates by purchasing more goods., which provides greater scale for the retailer who passes on the new savings as well. Yippee. This is why firms such as Costco enjoy sales per foot of retailing space four times greater than run-of-the-mill supermarkets. ‘Scale economics shared’ incentivises customer reciprocation, and customer reciprocation is a super-factor in business performance.”

ASOS is a pioneer in digital and customer obsessed (one of the first retailers offering free returns and a user-friendly site to buy clothes from). From my reading, this is what stands out:

ASOS provide a premier delivery service membership (free next day delivery) - this reminds me of a Costco membership or Amazon Prime.

ASOS didn’t pass on higher costs due to Brexit / Shipping issues to their customers - this is the kind of long term thinking that benefits companies in the long run.

ASOS aims to increase the revenue of their own branded goods to £1billion over the next few years - this is not too dissimilar to Amazon growing its own brand (Amazon basics).

It reminds me of the customer-centric Zappos (which incidentally was acquired by Amazon). ASOS could make quite a good acquisition for Amazon who could capitalise on making further efficiencies. ASOS now also own Topshop, Topman, Miss Selfridge, all acquired from the failed Arcadia Group. Having this additional real estate and the physical stores adds to their value and compliments, as well as diversifies their service offering and revenue.

What’s great

Profit

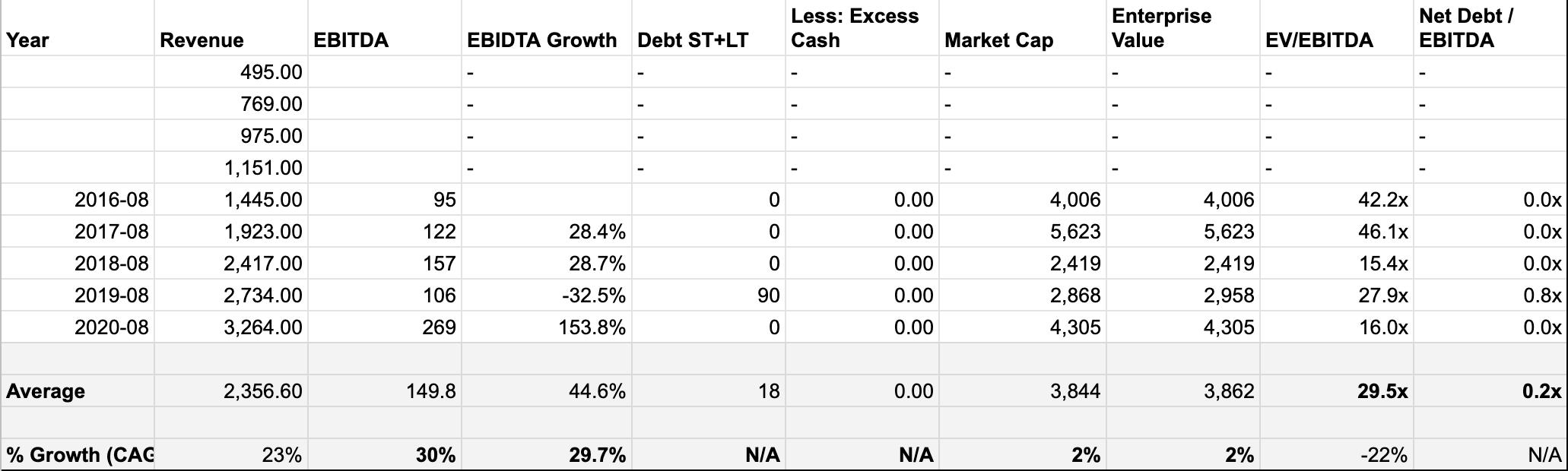

Topline revenue growth at a 23% CAGR in the last 5 years

EBITDA growing at 30% CAGR

Good gross profit margin at 50% and seems stable

Earnings per share are improving over a 10 year period

Good retained earnings growth, with 18% year on year average increase

Company

Current EV/EBITDA multiple looks cheap at 9.2x

Decent amount of cash and equivalents with 3.6x net income

Inventory is going up corresponding with revenue growth

Return on assets is good and defensible

Depreciation is low

Debt

Interest expense is low, currently at 6%

Net Debt / EBITDA is at 0x

No short or long term debt

What’s okay

Net earnings are low (but this may allow the company to grow)

CAPEX is high but not bad (86% of net income over 5 years)

Return on shareholder equity is good but not amazing

PPE costs are neither bad or low

The ratio of total liabilities & debt to shareholders equity is okay

What isn't great:

Sales, General and Administrative costs are as much as 92% of gross profit, which suggests a highly competitive industry

Analysis and price target

When looking at the financials below, we can see top line revenue has a 23% compound annual growth rate, which is amazing. We can also see EBITDA has been growing fast at an impressive CAGR of 30%. There’s also no debt. But what I like most is that we can see ASOS has an EV/EBIDTA multiple is at 16.5x, but at the current stock price this is actually now at 9.2x. This is quite low for this quality of business.

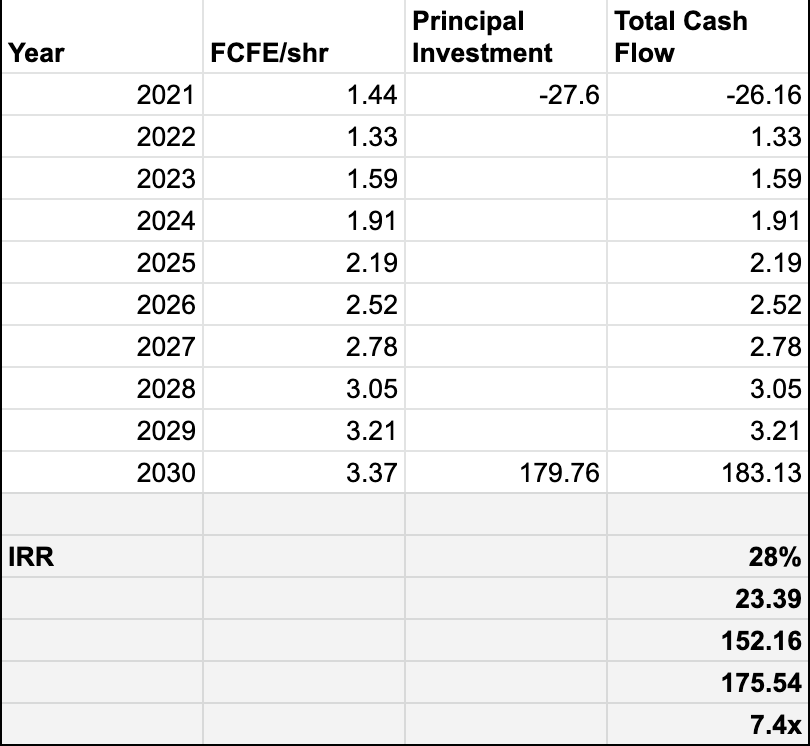

Let’s take a look at the free cash flow. This is also growing impressively at a 32% CAGR. ASOS do have plans to spend more on CAPEX in the next few years, so we’ll need to take this into account in our estimates. Therefore we also expect a low FCFE/yield.

Using a combination of analyst predictions and ASOS’s own targets, we’re looking at a EBIDTA having a 11% CAGR over time. This is much lower than what they have achieved in the past.

For the long term FCFE yield, we’ve used a low 2.5% as we’d expect due to their CAPEX spend. Our projected FCFE growth is similar or even less than the company’s own projections. Using the FCFE and EV models, we model the future share price at 183.13 in 2030, compared to the current price of 27.

We’re not using aggressive numbers but the IRR is extremely high at 28%. Even with this estimation, it has a market beating internal rate of return at 28% annual growth.

Our verdict

We think there’s a lot to like about ASOS. Their customer friendly stance is what we like in companies as well as their solid financials. Unfortunately their CEO left the company and is still needed to be replaced. This makes this investment less certain as it’s not definite we’ll see a continuation of performance. Furthermore, international expansion can be extremely difficult. Whether they can successfully leverage their retail stores, expand in other markets and keep up the growth is yet to be seen. Therefore, we’ll give this stock a 7/10 in confidence, but we think it could pay off if ASOS manage to meet their targets.

Giles Capital confidence score: 7/10

Long term hold (but sell if EV/EBIDTA value gets expensive historically)

Disclosure:

We have not purchased ASOS, but are keen to do so soon.

Disclaimer:

This is not investment advice. Our content to be used for informational purposes only. It is important you do your own analysis before making any investment based on your own personal circumstances.

About:

Sign up to our free newsletter for more analysis & recommendations:

Stay invested and follow Giles Capital on Twitter at @GilesCapital.

An updated version of this would be interesting