Our new investment idea: Hanesbrands Inc (NYSE: HBI)

Our new investment idea: Hanesbrands Inc (NYSE: HBI)

Over the last year, the market has been consistently affected by the consequences of lockdowns, inflation, and financial constraints, which have impacted various industries - particularly the apparel industry. This has resulted in supply chain disruptions and increased production costs, putting pressure on the global apparel market. Because of these challenges, some companies have become potential bargains. In this context, we will explore Hanesbrands Inc. in this write-up.

HanesBrands Inc

HanesBrands Inc (HBI 0.00%↑) is one of the leading companies in the apparel knitting mills industry in the US, with an annual revenue of $6.23 billion (USD), largely across their Inner-wear, Activewear, and International business segments.

Founded in 1901 by John Wesley Hanes, Hanesbrands started its journey as a world-recognised producer of seamless nylon hosiery and was acquired by the Sara Lee Corporation in 1979. Sara Lee Corp. decided to focus on transforming its portfolio, and as a result, HanesBrands Inc, which was considered a non-core business, was spun off in 2006. Since then, HanesBrands has emerged as a leader in the apparel industry and employed roughly 59,000 workers worldwide.

Comparative advantage

Looking at data from 2018 to 2022, Hanesbrands' average depreciation costs were approximately 5.2% of its gross profit. This suggests that the company has been investing in maintaining its durable competitive advantage and implementing its ambitious long-term plan for a sustainable future, which includes a focus on customer-centric e-commerce, ethical practices in its operations, and a recent initiative for proximity marketing.

With its aggressive M&A plan in expanding its market share in the activewear and Inner-wear segments over the past ten years, the company has planned ahead for its targeted future as stated in its “Full Potential Growing Plan”, and enhanced its competitiveness. Hanesbrands' 70% ownership of its sustainable supply chain, coupled with its highly horizontally integrated growth strategy, has enabled the company to establish strong relationships with retailers and manufacturers in the market. This has given the company an advantage in determining prices and has helped it to position itself as a leader in the industry. Meanwhile, Hanesbrands is seeking to adjust its capital allocation strategy in order to bolster its balance sheet and enhance its financial flexibility.

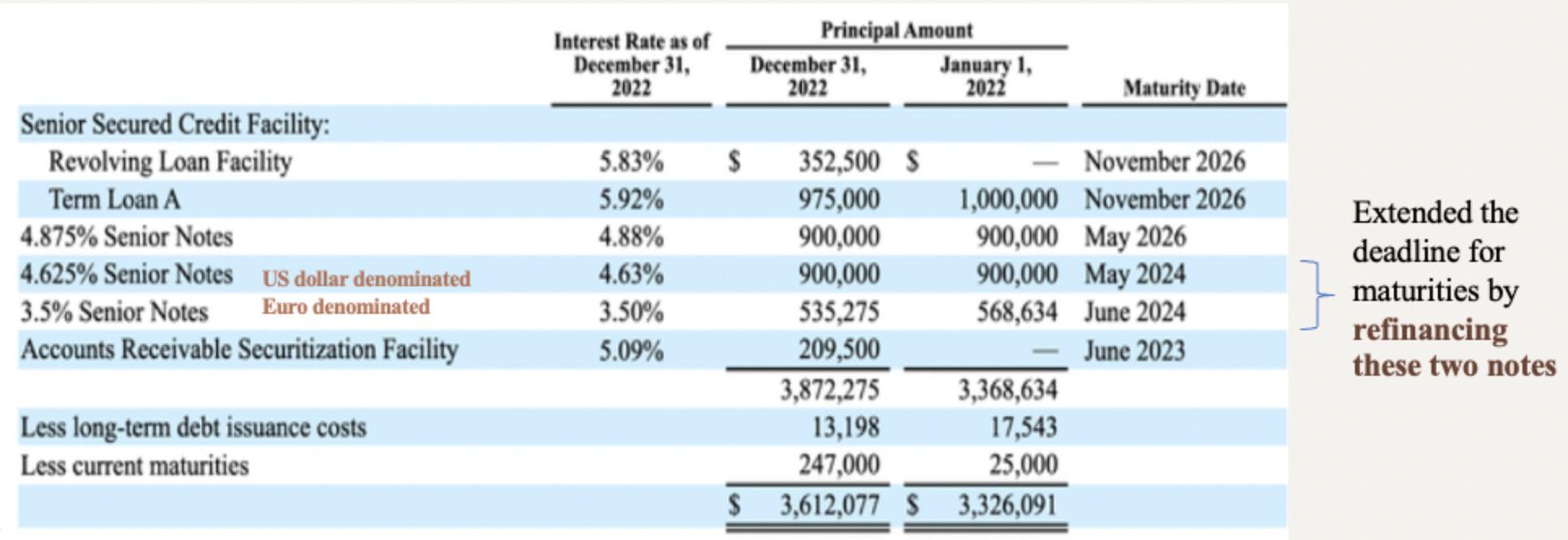

Concerns over debt

Hanesbrands faced challenges in recent years, starting with the acquisition of Europe Champion in 2016, which strained the company's cash flow. This was followed by unexpected events like the pandemic, supply chain disruptions, and a ransomware cyber attack crisis in 2022. The ransomware attack alone resulted in a loss of $100 million. These factors have made it difficult for the company to maintain its usual revenue generation after the acquisition. In 2023, Hanesbrands is experiencing a cause for concern as the ratio between its current assets and debt coverage is inadequate. This highlights the need for the company to take steps to address its debt levels and improve its financial position moving forward.

Looking at the longer term, Hanesbrands took action to address its debt levels by refinancing two of its notes and issuing a new $600 million senior note due in 2030. This was a strategic move aimed at navigating through the debt crisis and improving the company's financial position. By taking these steps, Hanesbrands has been able to reshape its strategic development goals and create an advantage from its challenges.

Higher Cash Generation

To improve its financial situation and reduce its debt, the company has taken some initial steps. Firstly, it has focused to reduce its inventory, which was causing a significant strain on its operating cash flow. Secondly, the company has made the unprecedented decision to cut its dividend. These two decisions should help Hanesbrands greatly improve its cash position and restore its flexibility in the market after the threats posed by the concerning debt issues. Hanesbrands itself has not underperformed compared with its peers considering the macro factors and the cyberattack accidents that negatively affected the figures during 2022.

Historically, Hanesbrands has demonstrated consistent performance, maintaining an average profit margin of 36.56%, even during economic downturns and global crises. Should its issues be temporary and be resolved, Hanesbrands could look undervalued and a patient investor may be able to reap the rewards from it.

What’s great

The average yearly net profit average over the last 10 years is 0.34 billion, which is 20% of its current market capitalization (1.7 billion).

$600 million stock buybacks program and higher current cash-generating ability with our IRR forecast of 23%.

Eliminated the dividend to free up the cash for debt reduction.

Depreciation is low at 5.2% which shows the company has made an effort to keep its durable comparative advantage.

What’s okay:

Inventory levels have been decreased by 6% compared to the previous year to reduce the operating cost.

Average Profit Margin of 36.35% and a consistent gross margin over the years.

Revenue has a CAGR at -2% over the last decade. While this is not great, we can see recent problems as temporary issues. The company has addressed these issues immediately and mitigated their impact going forward.

What isn't great:

18% decrease in brand sales on a reported basis as compared to 2021 attributed to a decline in American consumer spending.

High-risk exposure to debt from the aggressive usage of leverage, with current a Net Debt/EBITDA ratio of 5.2.

Net earnings are currently -2.04% of revenue with an average of 5.7%.

The company's profitability was lower than expected due to high operating costs, which accounted for an average of 76.16% of gross profits.

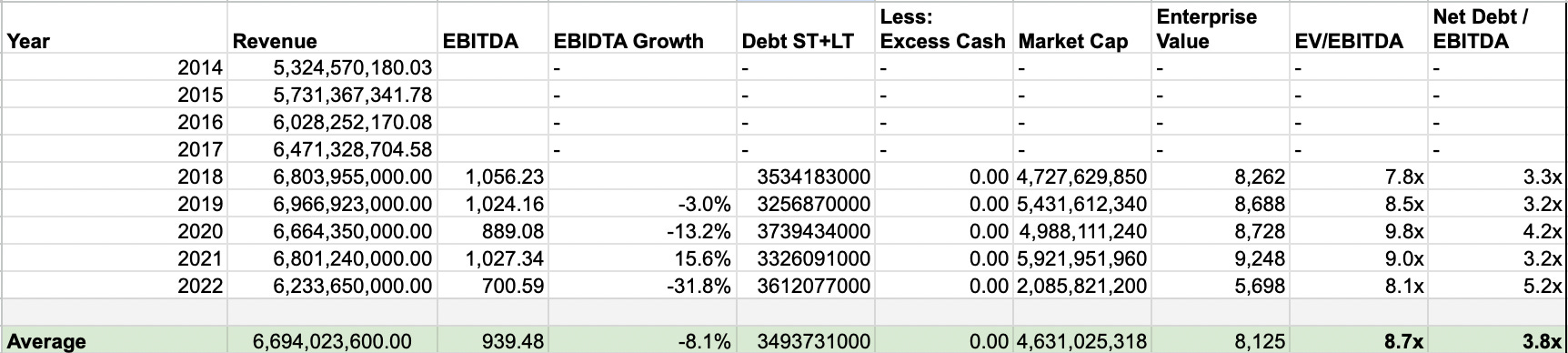

Revenue & PE ratio

An important indicator to evaluate the company growth is revenue. For Hanesbrands, revenue has underperformed at the CAGR of -2% over the last 10 years due to the negative impacts from the pandemic, supply chain problems and the previous cyber attack during the past three years. However, we assume this underperformance is a blip rather than a trend.

If we exclude the impact of the pandemic from our analysis, it is likely that Hanesbrands’ revenue will remain stable or even increase slightly compared to historical data. Its EV/EBITDA ratio is a near consistent 8.7x average historically and the company’s future performance is still predictable to a certain degree. If the EDITBA returns to normal, at the current valuation it would have an EV/EBITDA as low at 5.2x.

Compared to other companies, Hanesbrands may look like a weaker choice due to its high Net Debt/EBITDA ratio which indicates that it is over-leveraged. However, if we assume revenue improves and again with its current market value, this would be a Net Debt/EDITDA ratio of 3.5x.

Over the last 10 years, Hanesbrands has an average of PE ratio of 13.9. If the earning per share would return back to normal, and at its current price of around 4.96 dollars per share, Hanesbrand would have a current PE ratio of only 3, which is extremely cheap and it might have the potential to grow later on as an undervalued security.

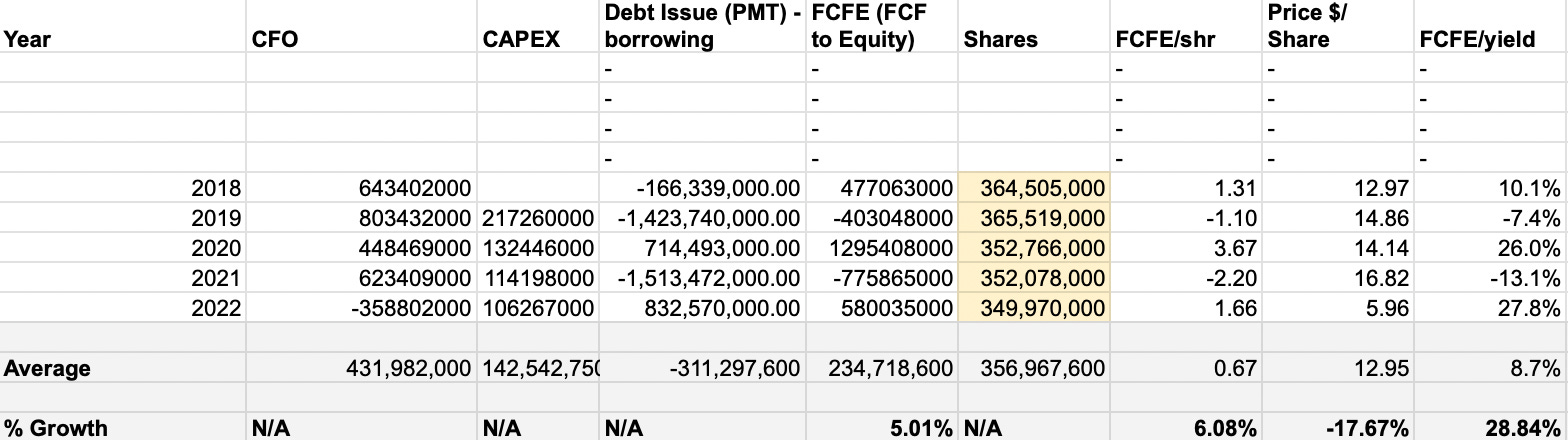

Share count and cashflow

It is positive to see the number of outstanding shares go down in the last 5 years, benefiting the shareholder. Regarding the cash flow, although not stable, on average it returns about 6.08% of FCFE/yield every year, which is decent.

Forecast

For an assessment on the company’s future value projection, we have made two assumptions:

Assumption One — The aftermath of the COVID-19 is assumed to be none

Assumption Two — The profitability of the company returns back to normal.

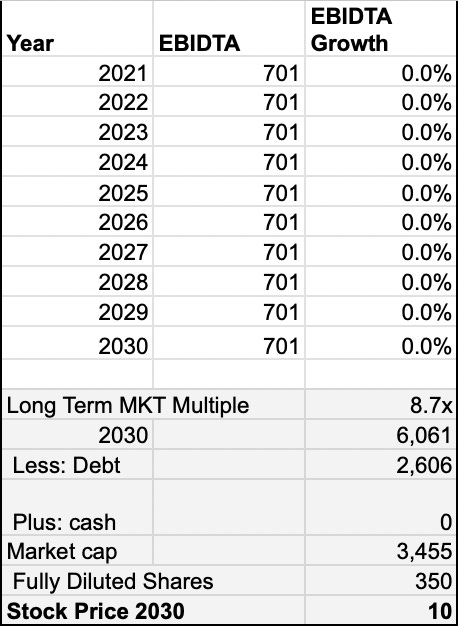

If these are true, we could start to forecast using conservative numbers. From the EV multiple forecast, even if we assume EBITDA won’t grow, based on the average market multiple of 8.7x, it would give us a target stock price of 10 by 2030.

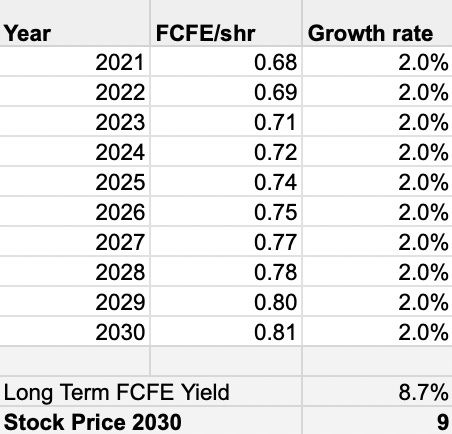

For our FCFE forecast, we use the average FCFE/share of 0.68 for the last 5 years. Let’s assume it grows at a rate of 2% a year. This gives us a target stock price of 9 dollars per share.

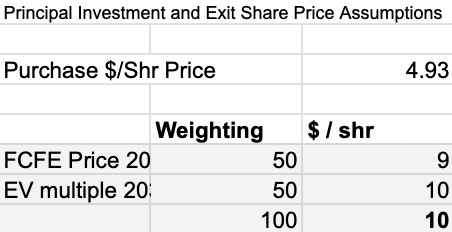

We can purchase the stock at 4.93 dollars today. When we average out our FCFE and EV multiple forecasts, we get a target price of 10 dollars per share.

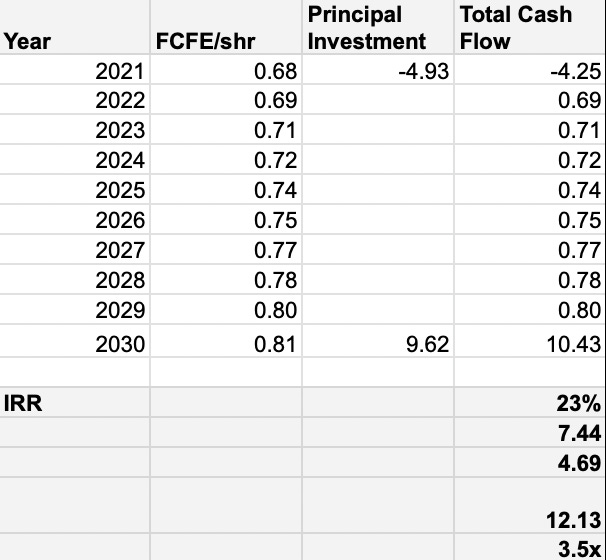

Adding the FCFE/Shr back we model the future share price at 10.43 dollars per share in 2030. This equates to an IRR of 23% which is market-beating.

Summary

Hanesbrands has been grappling with a range of challenges in the aftermath of the pandemic, including supply chain and inventory issues stemming from prolonged inflation, weaker consumer demand, lower sales, and higher operating costs. In addition, the company has faced cash flow problems following a major acquisition and a ransomware cyber attack in 2022, which have further strained its finances and raised concerns about its debt levels.

In response, the company has decided to implement a stock buyback program and retain more of its income in an effort to improve its financial position and address these challenges going forward. It is our belief that Hanesbrand's stock is currently both misunderstood and mispriced, and we believe that in due time the true value of the stock will be revealed. However, it remains to be seen how the market will react and whether our assessment will prove accurate.

Giles Capital confidence score: 7.5/10

This is a fairly high confidence score and we would look to buy and hold over the long term as Hanesbrand sets to be revalued in line with the rest of the market.

Disclosure:

We currently hold a position in Hanesbrand.

Disclaimer:

This is not investment advice. Our content is to be used for informational purposes only. It is important you do your own analysis before making any investment based on your own personal circumstances.

About:

Sign up to our free newsletter for more analysis & recommendations:

Stay invested and follow Giles Capital on Twitter at @GilesCapital.