Our new investment idea: FPT Corporation (HOSE:FPT)

Our new investment idea: FPT Corporation (HOSE:FPT)

Every month we'll be sharing a breakdown on our investment ideas. Previously we’ve discussed potential investment ideas such as Constellation Software in Canada and West Japan Railway Company in Japan. Today we’ll discuss our potential investment in FPT Corporation in Vietnam.

FPT Corporation (HOSE:FPT)

FPT was founded in 1988 as 'The Food Processing Technology Company' operating in the fields of drying technology, information technology and automation technology. Fast forward 34 years and FPT Corp is now the largest IT services company in Vietnam and among the top companies to work for in Asia. It has annual revenue of 1.3 billion USD and a market cap of 3.7 billion USD.

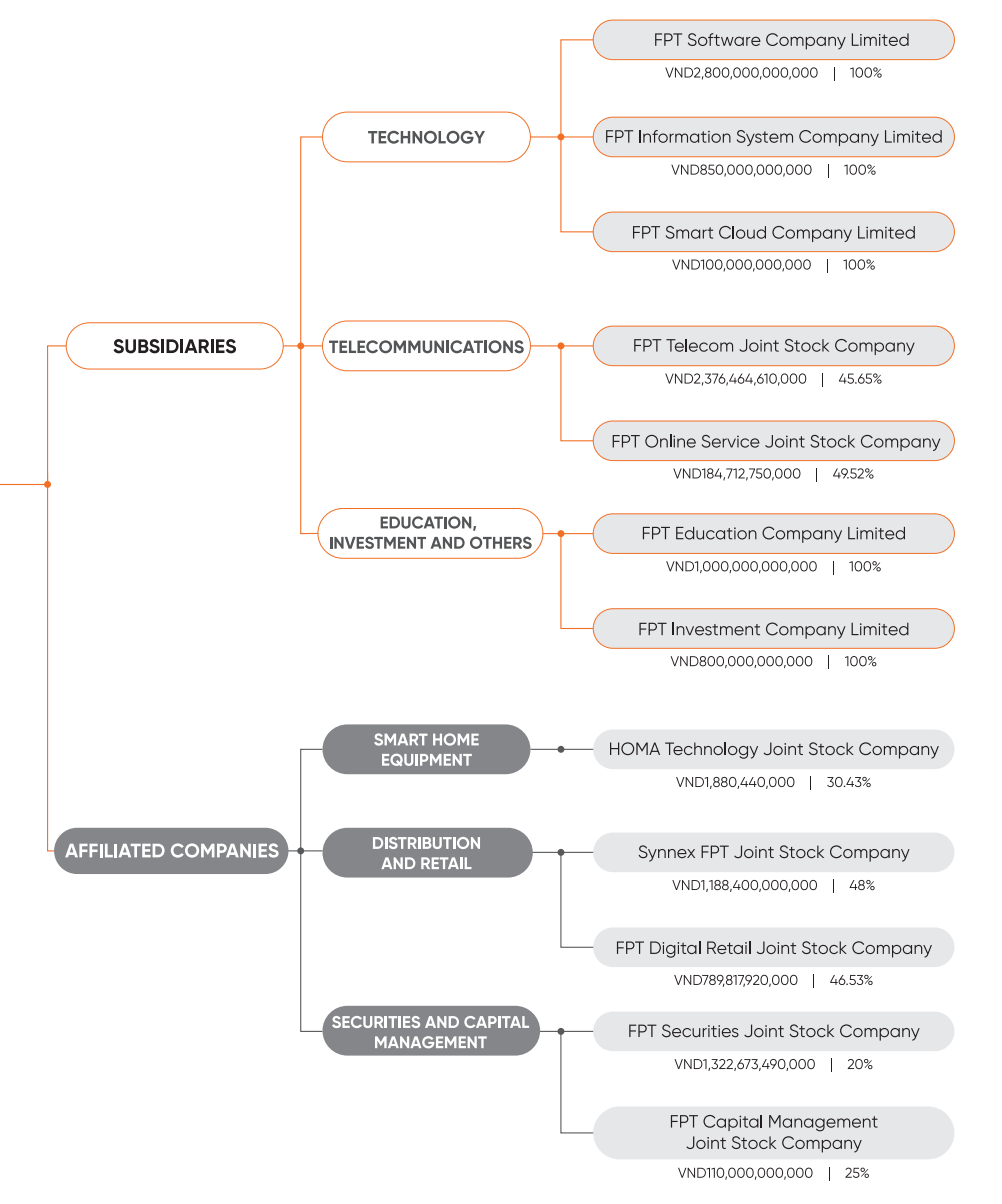

FPT’s key sectors are information information technology (56% total revenue), telecommunications (39% total revenue) and education (7% of revenue). A full breakdown of its subsidiaries and affiliated companies is shown below. FPT Corp undertakes software development for many foreign clients, with half of these orders coming from Japan. In the last few years FPT has focused on shifting from being an IT service provider to being a DX (digital transformation) service provider. It is also moving more into AI, big data and cloud computing services.

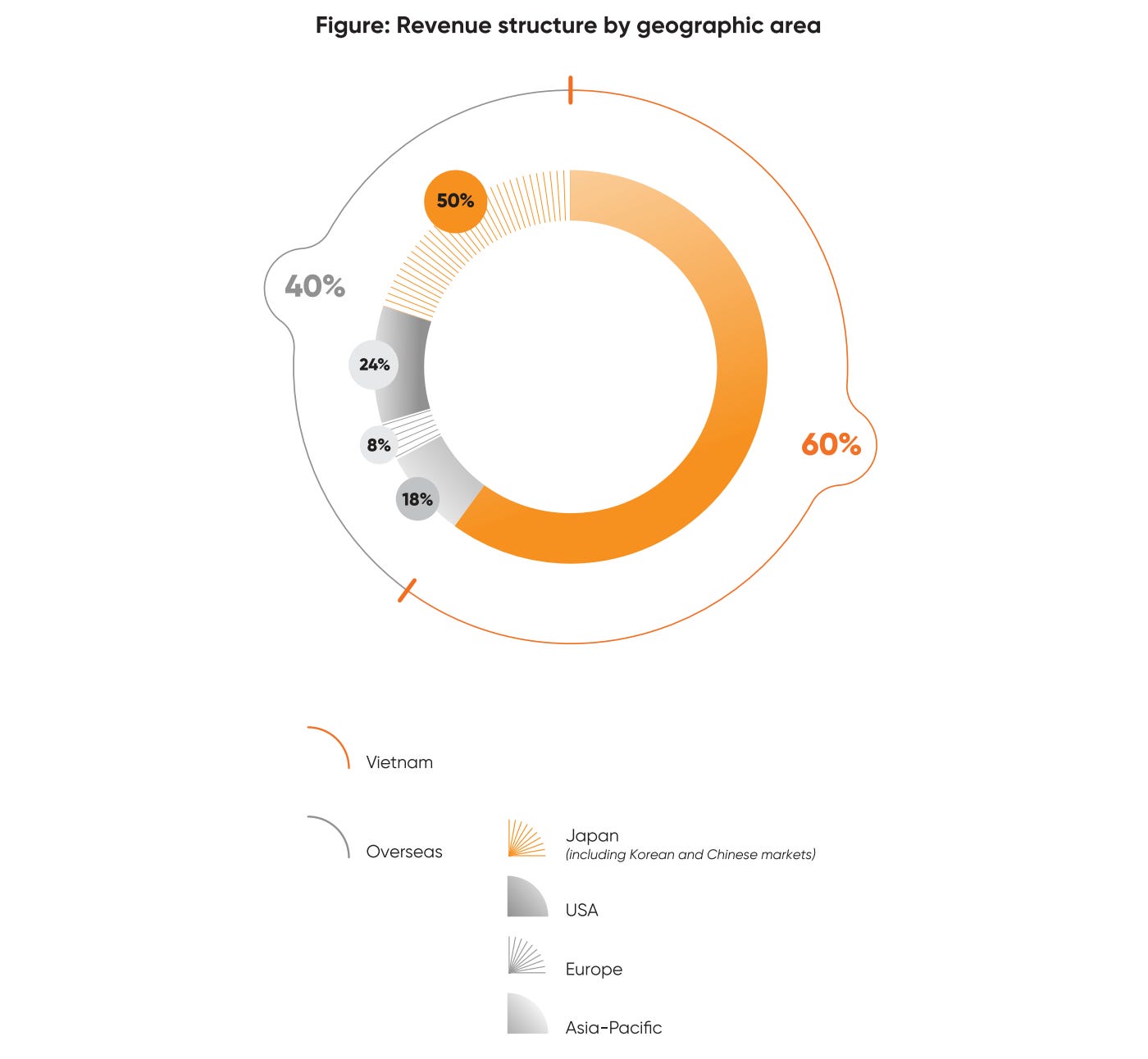

FPT notes that 72% of small to medium enterprises in Vietnam want to go digital, compared to 32% in 2019. However, it would be wrong to think of FPT as only a domestic company with operations in 26 different countries, which make up to 40% of its revenue.

FPT’s last annual report shows the company grew 8-9% in key markets such as Japan and US and grew an impressive 28% in Asia pacific. So far it looks as though FPT’s strategy moving into DX has proved successful home and aboard with strong trends in digital transformation during this Covid-era. Let’s look at how this growth appears in the financials.

What’s great

Profit

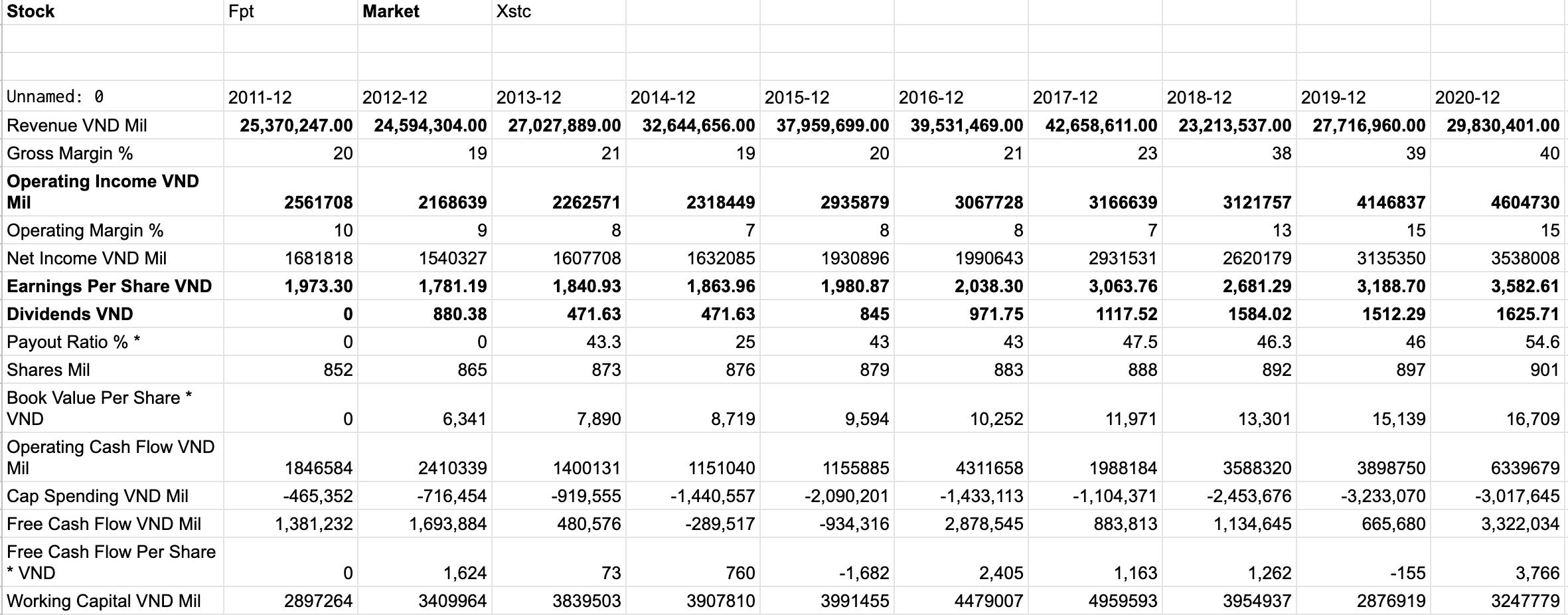

Gross margin has grown from 20% to 40% in the last decade. This suggests it has a growing competitive advantage.

Net earnings as percentage of revenue have almost doubled from 6.6% to 11.86% in the last decade, which is good.

EPS has also consistently grown most years from 1,971 VND to 3,582 VND over the last decade.

Retained earnings has been growing on average 7.5% per year in the last 5 years which is great.

Company

Depreciation on average is around 12% of gross profit, which is fairly good.

Total return on assets is on average 9% which is good as it may suggest a higher barrier to entry for new competitors.

Shows an average return on shareholder equity of 22.5% in the last 5 years, which is great.

Property, plant and equipment costs are low. It can pay for it with around 3 years earnings.

The company does not need to spend on R&D and has low capital expenditure.

Presence of treasury stock on the balance sheet.

Debt

Interest expense is recently very low at around 8% of operating income which fantastic.

No long term debt, although short term debt is growing. This is not concerning due to its excess cash is more than the debt.

What’s okay

Cash and cash equivalents are equal to 1.3x its recent net earnings.

Amount spent on Sales, General and Administrative is at 61%, however it is trending down slowly.

Treasury share adjusted debt to shareholder equity ratio is 1.65, which is okay.

What isn't great:

At current price the stock has a PE ratio of 26, which isn’t low

At current stock price, the company has an EV/EBITDA multiple of 11.7 which is not bad but it is higher than previous years.

Revenue & PE ratio

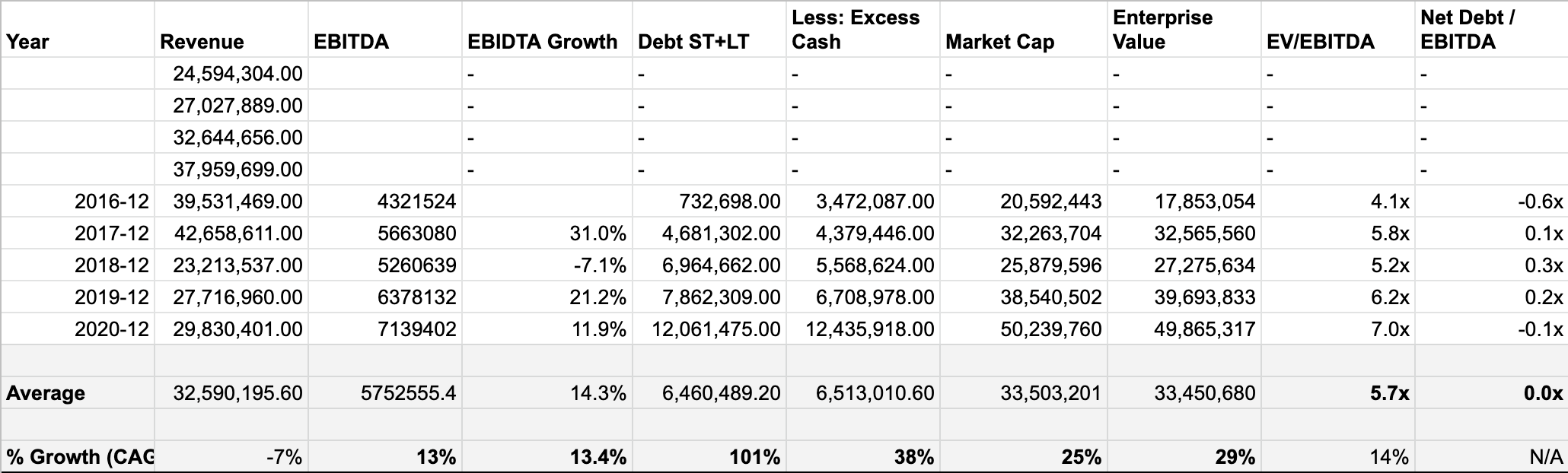

When looking at the financials below, the revenue looks as though it peaked, then collapsed. This is actually due to FPT selling a 47% stake in its trading arm to Taiwan's Synnex Technology in 2017. We can see that EBITDA has actually increased throughout this period at around 13% a year and that revenue is climbing up again.

FPT’s average EV/EBITDA ratio would be 5.7x. However, taking the current stock price, and previous earnings its EV/EBITDA ratio would be at 11.7x. Furthermore with the current stock price and previous earnings its PE ratio would be 26, but the average PE ratio in the last 5 years has been 13. Unfortunately the stock has been cheaper in the past but its EV/EBITDA ratio is fair. Its also worth noting the company has no debt overall.

Cashflow

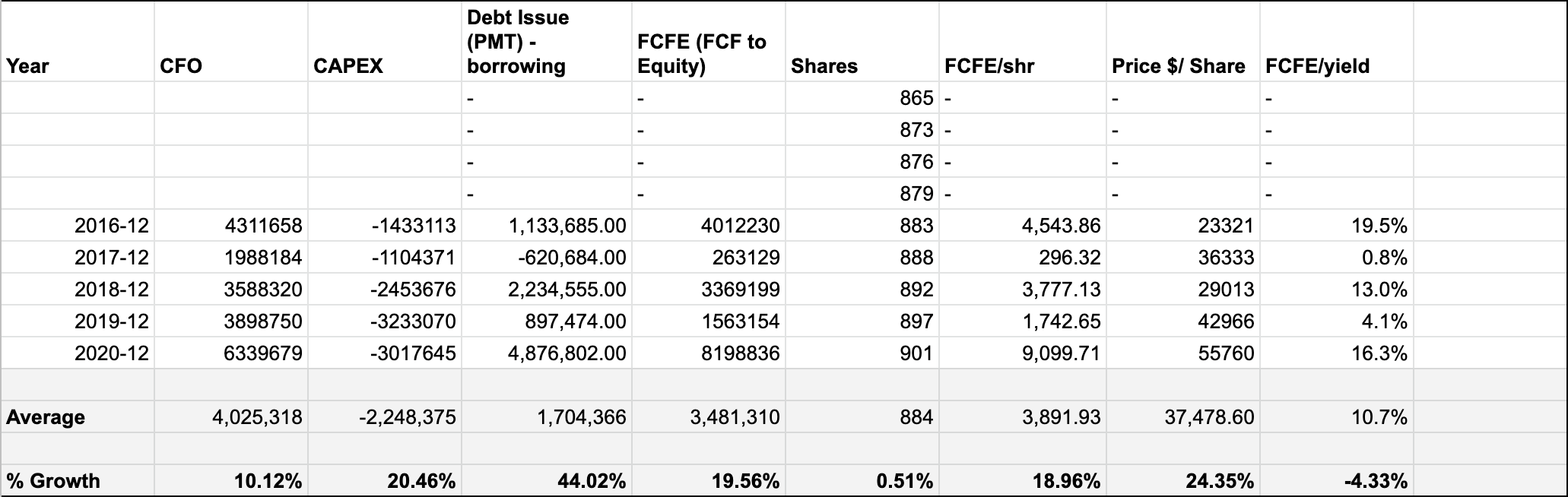

Let’s take a look at the free cash flow. We can see quite a stable free cash flow being produced. That’s an average of 10.7% FCFE/yield every year, which is very decent.

Forecast

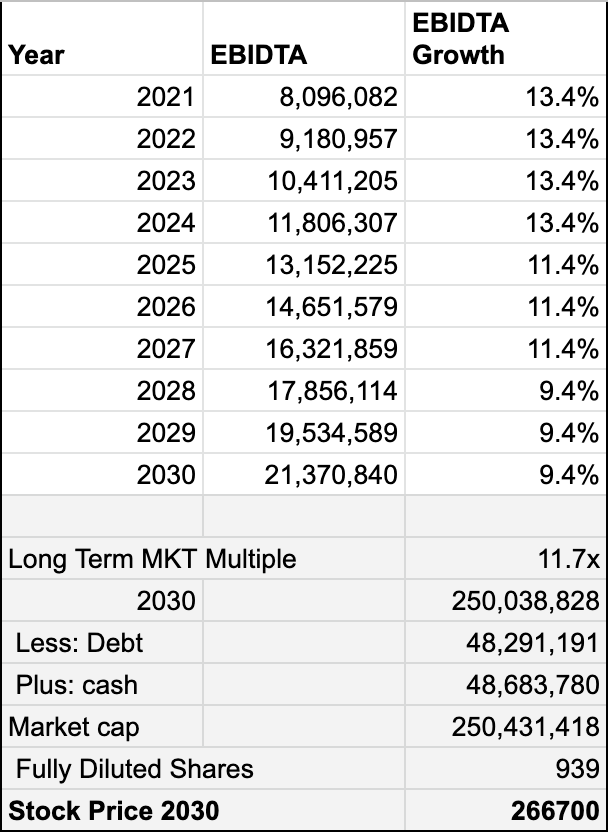

For our EV multiple forecast, we can assume EBITDA will grow. We’re going to use the average of the last 5 years at 13.4% and assume it slows down. We use a current long term market multiple of 11.7x. This gives us a target stock price of 266,700 dong:

For our FCFE forecast, we use the an average FCFE/share of 3891 of the last 5 years. Let’s assume a it grows at a rate of 13.4% a year. This gives us a target stock price of 108,486 dong.

We can purchase the stock at 91,300 dong today. When we average out our FCFE and EV multiple forecasts, we get a target price of 187,593 dong.

Adding the FCFE/Shr back we model the future share price at 199,242 dong in 2030. This equates to an IRR of 15% which is market beating. We’re not using aggressive numbers and we could see this easily outperforming an IRR of 15%, particularly given the company's good management and focus on digital transformation.

Summary

FPT Corp generates a lot of cash and many parts of the business are growing well. It is relatively inexpensive and could be a great investment for those who want a reasonably priced stock which bets on the continuation of digital transformation.

Giles Capital confidence score: 8/10

This is a high confidence score and we would look to buy and hold over the long term as FPT looks to become a premier IT consulting company.

Interested to do your own analysis?

Check out our GCS tool that helps you pull in data so you can do your own analysis in Google Sheets. This is what we use to analyse companies financials statements.

Disclosure:

We currently do not hold any positions in Vietnam but would like to increase our exposure to emerging markets.

Disclaimer:

This is not investment advice. Our content to be used for informational purposes only. It is important you do your own analysis before making any investment based on your own personal circumstances.

About:

Sign up to our free newsletter for more analysis & recommendations:

Stay invested and follow Giles Capital on Twitter at @GilesCapital.