Our new investment idea: Ferrexpo Plc (LON: FXPO)

Every month we'll be sharing a breakdown of our investment ideas. Previously we’ve discussed potential investment ideas such as Hanesbrands and Turtle Beach Corporation in the USA. Today we’ll discuss our investment in Ferrexpo in Ukraine.

Ferrexpo Plc (LON: FXPO)

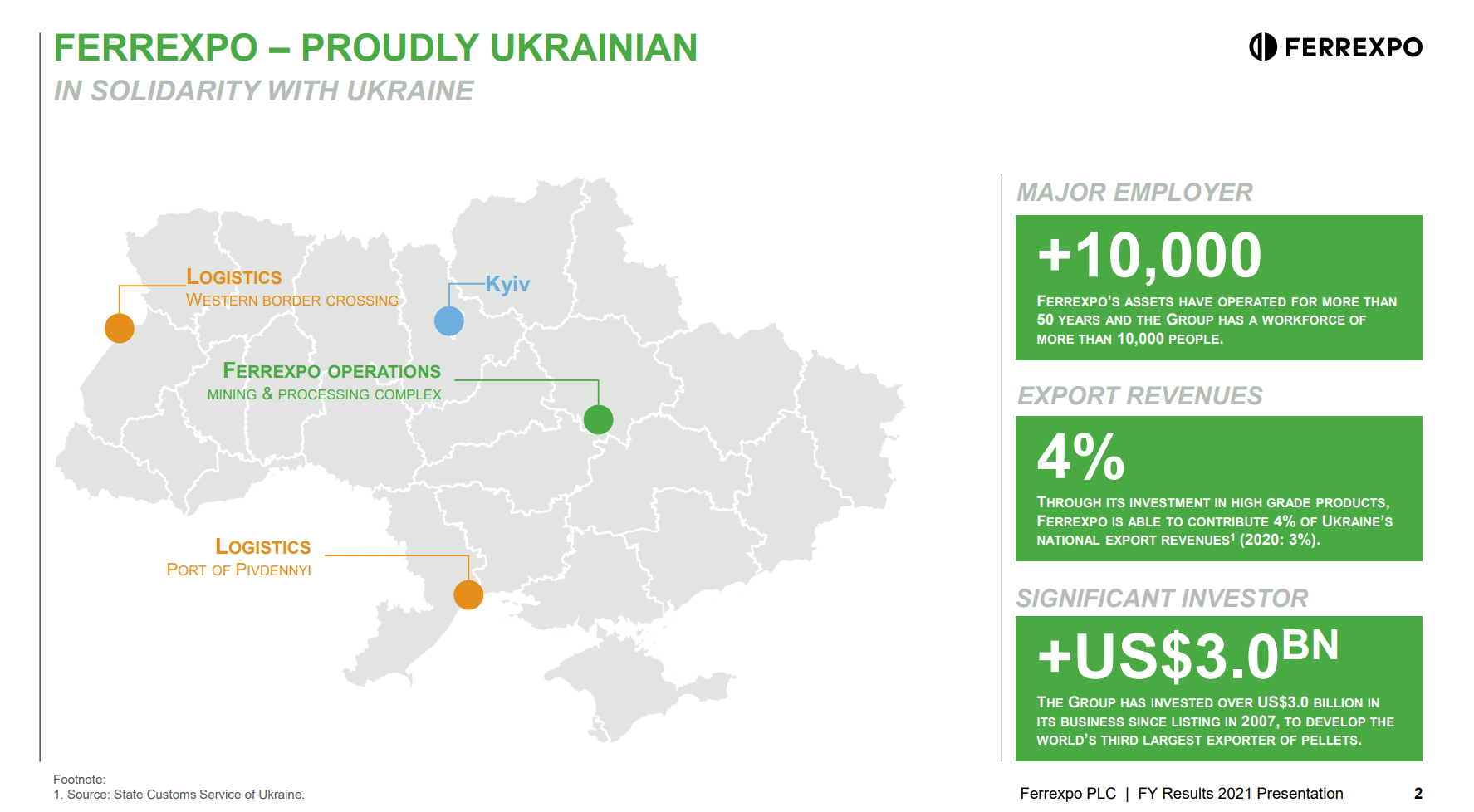

Ferrexpo was founded in 2002 and is now one of the largest iron ore producers in Ukraine. Ferrexpo is headquartered in Baar, Switzerland, and is listed on the London Stock Exchange. However, Ferrexpo's primary assets and operations are located in Ukraine, where it has iron ore mining, processing, and logistics facilities. Ferrexpo's business is the mining and beneficiation of iron ore into high-grade pellets for sale to the global steel industry. In 2021, Ferrexpo generated revenues of $2.5 billion (USD) and produced 10.5 million tonnes of high-grade iron ore pellets.

Ferrexpo had previously invested in expansion projects to increase its production capacity. The company arguably has a significant competitive advantage with its large, high-quality iron ore reserves, low-cost mining operations, and strategic location.

The company has three open pit iron ore mines near the city of Kremenchuk in the Poltava region of central Ukraine, along with processing facilities and a logistics infrastructure including its own rail wagons and port. Ferrexpo did export the majority of its iron ore pellets to steel mills in Europe, the Middle East, and Asia.

Ukraine war and its impact on Ferrexpo

Ferrexpo's share price has fallen over 60% in the past year. The conflict between Ukraine and Russia has created significant uncertainty for Ferrexpo's future operations, temporarily limiting access to certain logistical routes. Ferrexpo has worked to maintain operations while prioritizing the safety and security of its workforce.

Ferrexpo's assets have not been damaged and are located in the Poltava region, which is fairly far from the current front line. Positively, its net cash position and the absence of material financial debt make it more resilient than other Ukrainian corporates.

However, Ferrexpo has been using railway and river barges as its main export avenues since the outbreak of the war due to the closure of Black Sea ports, which used to account for 50% of its export sales. Ferrexpo's export capacity has reduced materially from pre-war levels while logistical costs have increased due to these bottlenecks. This has led to a significant drop in revenue and net income.

Another persistent issue is the court cases that the Ukrainian state authorities have brought against the company and its main shareholder, Kostyantyn Zhevago. The Ukrainian court seeks to seize billionaire Zhevago's Ferrexpo shares. Ferrexpo sold previously purchased treasury stock shares from the market to a third party, reducing the nominal share of Kostantyn Zhevago in the company to 49.5%. This makes the transfer of control of Ferrexpo to the Ukrainian government unlikely. Zhevago has vowed to appeal the rulings, maintaining that the cases are politically motivated.

The outcome of both the war and the legal fight remains uncertain but presents risks for both the ownership control of Ferrexpo and the company's ongoing operations during an already turbulent time. Despite all of these headwinds, let’s look at the financials to get a complete view of the business.

What’s great

Profit

Strong gross profit margin over the past decade, with a 10-year average of 59.9%. Prior to the war in Ukraine, Ferrexpo's gross margin reached 71% in 2021, indicating very profitable operations.

Selling, general and administrative expenses (SGA) relatively low in recent years. Over the past 5 years, Ferrexpo's average SGA as a percentage of gross profit has been 35%, which is considered good for the industry.

Stable net earnings over the past decade, with the 10-year average sitting at 28% of revenue. This consistency is positive, and net earnings have shown an upward trend in recent years, increasing from 20% in 2016 to 35% in 2021, indicating improved profitability.

Ferrexpo's retained earnings have been steadily increasing over the past few years, suggesting a competitive advantage.

Company

Has an average depreciation of 9.4% of gross profit over 5 years, which is good for a mining company.

With over 50 more years of iron ore reserves at current mining rates, Ferrexpo does not need to dedicate major resources to R&D and can focus its capital on maintaining efficient production and logistics and should generate a lot of cash for the business.

With cash and cash equivalents averaging around $200 million over the past 5 years, Ferrexpo has maintained a robust cash position, evidenced by its cash holdings representing over 28% of the company's current market capitalization of $704 million.

With average annual net earnings of $400 million, Ferrexpo can pay off its property, plant and equipment in 2-3 years, demonstrating a strong capacity for self-funding capital expenditures.

Ferrexpo has maintained a healthy return on assets over the past decade. The company's average ROA has been around 15% over the last 10 years.

Ferrexpo has maintained a high return on shareholders’ equity, which averaged 35% over the last 5 years.

Capital expenditure is low with Ferrexpo using 11% of its total earnings for capital expenditure on average over the last 5 years.

At current stock price, the company has an EV/EBITDA multiple of 1.06 which is much lower than the average of previous years of around 3.7.

Debt

The average interest expense has been 3.93% of its revenue over the last 5 years. This below-average interest expense is positive for Ferrexpo, indicating manageable debt levels and an efficient capital structure with minimal reliance on high-interest debt financing.

Overall Ferrexpo has only minimal debt linked to leases, which allows it to maintain a net cash position.

What’s okay

Ferrexpo's EPS has varied over the past decade but has generally remained stable with an average of $0.50-$0.60.

Inventory has risen from $160 million to $240 million since 2017, reflecting increased production and storage capacity. As iron ore pellets do not degrade in quality over time (if stored properly), the additional inventory could be sold if export routes in Ukraine reopen.

At the current price, the stock has a PE 3.1, but has a 5-year average of 3.7. However, if normal export routes return, the stock would have a PE ratio of 1.2.

What isn't great:

Ferrexpo has not conducted any share buybacks in recent years and its shares outstanding have remained relatively stable over the past 5 years.

The conflict in the region is creating large uncertainty around the company's operations.

Ferrexpo’s revenue and net profit are largely linked to iron ore prices and steel demand which could be uncertain in the future.

A resilient business

Despite the severe challenges posed by Russia's unprovoked invasion and ongoing aggression, Ferrexpo has shown remarkable resilience and adaptability to continue operating through this crisis. The company has managed to maintain partial production and profitability even amidst wartime disruptions and uncertainty.

Ferrexpo's operating capacity has improved substantially from the fourth quarter of 2022 when it dropped to just 15% because of power supply issues. The company is now operating at 35-40% of total capacity, a significant recovery compared to the major reduction seen previously.

Here we have a company that is debt-free with a market capitalization of £539 million but with £106 million in net cash in hand. During the war, Ferrexpo generated a net profit of £171 million. While profitable, this is lower than its pre-war profits (its 10-year average was £340 million.

The fact that Ferrexpo remained profitable during the difficult war period in Ukraine demonstrates the company's operational resilience and ability to navigate challenging conditions. With its shares trading significantly below pre-war levels, Ferrexpo now looks undervalued relative to its demonstrated resilience and fundamental business strengths.

Risks and rewards

Risks

Russian attacks pose obvious risks to Ferrexpo's operations. Indiscriminate bombing near Ferrexpo's assets threatens key facilities and equipment, potentially forcing extended shutdowns that would severely hurt revenue, finances, and the stock price.

Ferrexpo also faces risks from declining iron ore prices. Prices have fallen sharply due to reduced output and demand concerns at Chinese steel mills. China's Yunnan province ordered steel companies to curb production to meet government mandates, which combined with tepid post-COVID demand, reduces China's iron ore demand. As China accounts for over half of global steel output and ore demand, this downward pressure on prices could squeeze Ferrexpo's revenue and profits.

Rewards

However, in line with our perspective, Ukraine now poses an ever more difficult situation for Russia. Russia may struggle to make further advances as several Russian generals have been killed in the war or removed for speaking out. NATO looks to be expanding, and Ukraine now matches or exceeds Russia's armaments. Retaking minefields left by retreating Russians seems Ukraine's main obstacle.

Ukraine's measured counteroffensive seems wise, slowly wearing down opposition forces deployed for over a year without relief. Successful strikes beyond the frontlines mirror Russia's Kherson retreat. Putin's misjudgments have put Russia in a precarious position, and the conclusion may come sooner than expected.

De-escalation of Russia's operations, allowing logistical routes to reopen and reduce risks, could help. Exports through alternative routes are gradually increasing, though profits are far below pre-invasion figures.

Far afield Ferrexpo may also benefit from challenges facing African competitors. Africa's largest iron ore miner is building up stockpiles due to railway issues, indicating potential difficulties supplying customers.

Summary

In conclusion, Ferrexpo presents a compelling investment opportunity given its strong financial performance, competitive advantages, and attractive valuation. While the geopolitical risks associated with its operations in Ukraine are a concern, we believe that a contrarian may see Ferrexpo with potential upside.

If geopolitical tensions ease, Ferrexpo's financial performance could improve significantly from currently depressed levels. Iron ore prices may also recover over time as demand rebalances with supply, particularly with the rebuilding needs in Ukraine.

Ferrexpo's proven low-cost production, substantial reserves, and experienced management suggest the business can survive short-term volatility. For patient investors, the potential reward may outweigh the clear risks.

Giles Capital confidence score: 6.5/10

We have a moderate confidence level in Ferrexpo given the considerable uncertainty. But at such a low valuation, a small improvement in operating conditions could yield a substantial upside. We would look to make a small investment given the high-risk, high-reward profile.

Disclosure:

We currently hold a small position in Ferrexpo.

Disclaimer:

This is not investment advice. Our content is to be used for informational purposes only. It is important you do your own analysis before making any investment based on your own personal circumstances.

About:

Sign up for our free newsletter for more analysis & recommendations:

Stay invested and follow Giles Capital on Twitter at @GilesCapital.

Brilliant find mate. I especially loved how you segregated the good, bad & the ugly.

Overall thoughts - Though there are corporate governance issues, management has been paying fair dividends over the years. Even accounting for the worst earning year in the last decade (2015), we still get a 10% earnings yield.

Prima facie, looks compelling.

You didn't understand me - I wanted to say that your company/stock writeup was good 😊 but the "front line part" was crappy as you obviously believed the official western propaganda too much.