Our new investment idea: Airtel Africa (LON:AAF)

Our new investment idea: Airtel Africa (LON:AAF)

Every month we'll be sharing a breakdown on our past or present investments. Previously we’ve discussed our investments in Magna International in Canada and The a2 Milk Company in New Zealand. Today we’ll discuss our potential investment in Airtel Africa.

Airtel Africa (LON:AAF)

Airtel Africa provides telecommunications and mobile money services in 14 countries in Africa - primarily in East, Central and West Africa. Airtel Africa is majority owned by the Indian communication services company Bharti Airtel. It’s a fast growing company with its customer base increasing 24% in the last year. Its Airtel Money service has also been a success, operating in countries with poor banking access - this side of the business has grown 29% per year. Let’s take a look at what we see in the financials of the business.

What’s great

Profit

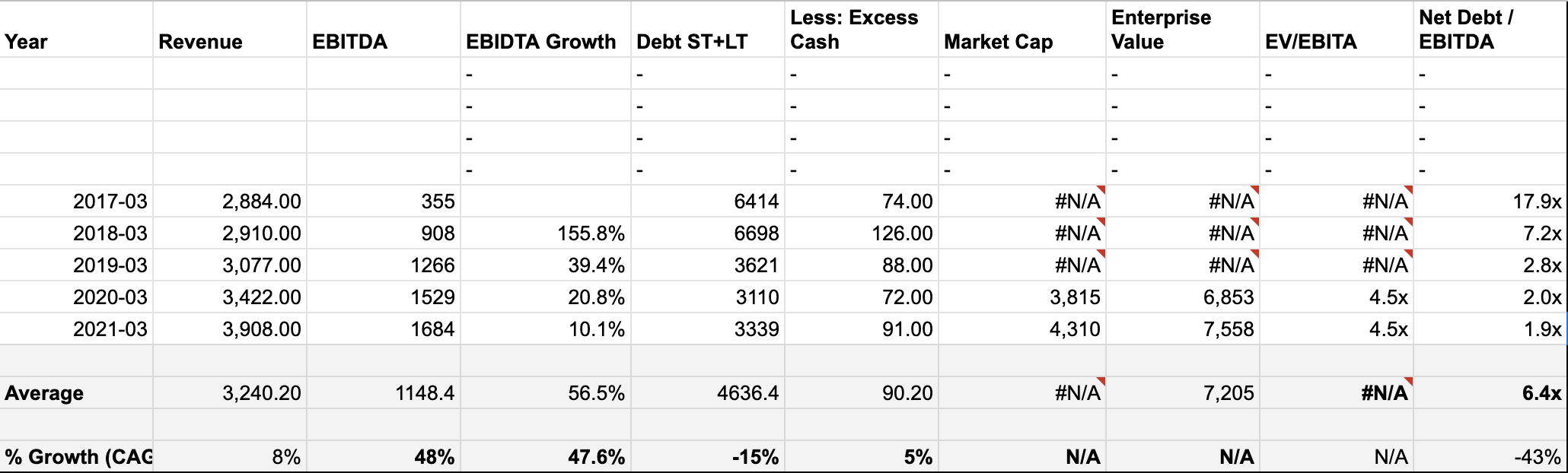

Top-line revenue growth has a CAGR of 8% and looks like its accelerating

Gross margin is great at 64% and seems to be increasing

Growing EBITDA with a CAGR of 48%

Retained earnings look good and have the potential to grow in the future

Company

Sales, General & Administrative costs are low at 25% of gross profit and looks like it is getting lower

Return on assets are low but at least the assets can be seen as defensible

Cash and equivalents look decent - it has the cash to ride things out

EV/EBITDA ratio is very decent at a 4.5x multiple

Debt

Interest expense is low at 8% of revenue

Net debt / EBITDA is good, at a low 1.9x

Debt is being reduced over time

What’s okay

Net earnings are 8-13% of earnings, which suggests its in a competitive business environment

Pays out a dividend of 2.91% a year

Earnings per share are stable and looks as though its slightly improving

Inventory is going up, but does not correspond with the rise in revenue

Short term debt ratio is acceptable but not low

Long term debt is not too high, it can pay it off with 5 years earnings

What isn't great:

Depreciation is high at 93% of gross profit, but it is getting lower every year

PPE costs are high and it would take the company 10 years to pay for it

Return on shareholders equity isn’t high

Debt to shareholders equity ratio is a bit high at 1.93

Capex spending is rather high

Goodwill is reduced over the years so its not acquiring good companies

Analysis and price target

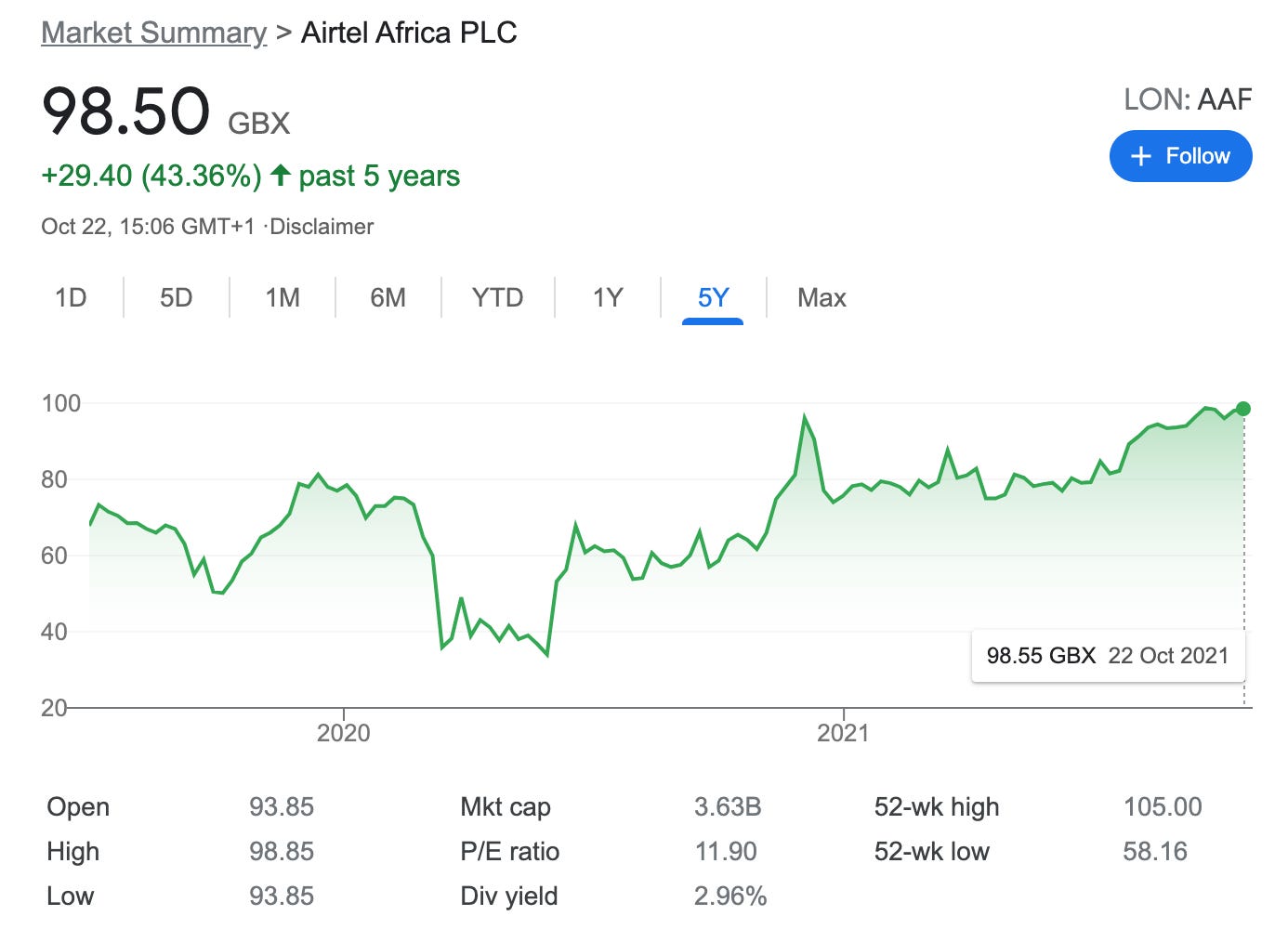

Airtel Africa had its IPO last in the summer of 2019. The price dropped after IPO and again after the first outbreaks of COVID. It is now 22% higher than its debut, but appears to still be good value with a P/E ratio of 11.90.

The first quarter of 2021 shows signs of growth, as revenue grew 53.7% year over year, driven by a 24.6% growth in customer base to 23.1 million. When looking at the financials below, we can see a top line revenue with an 8% compound annual growth rate which is good. We can also see EBITDA has been growing fast, at an impressive CAGR of 47%. Debt has been significantly been reduced over time too. But most impressive in my mind is that we can see Airtel Africa has an EV/EBIDTA multiple is at 4.5x. This is one of the lowest we’ve reviewed - for comparison Google has an EV/EBIDTA multiple of 28x.

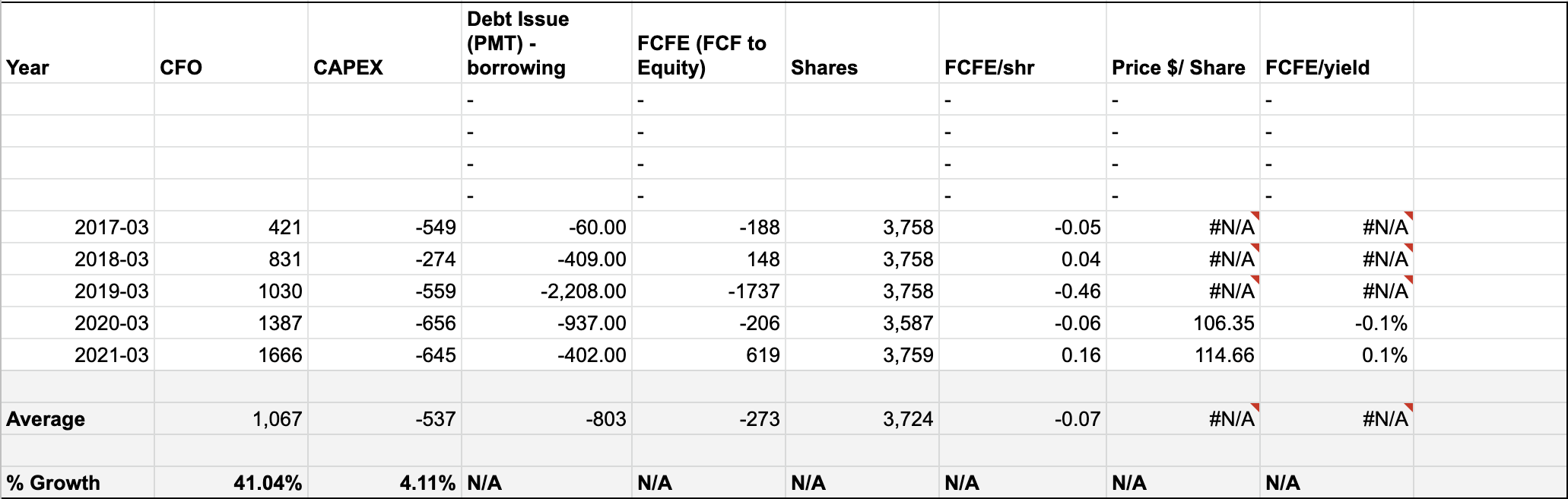

Let’s take a look at the free cash flow. This is also growing impressively at a 41% CAGR. Airtel Africa seem to be spending more, so per share this has only improved slightly, but ideally we would want more data here to make any judgements.

Unfortunately we only have two years of stock price data and six of financials, so I am less confident about modelling the price. However, using the FCFE and EV models, we model the future share price at 302 in 2030, compared to the current price of 98. This is using conservative growth numbers and assumes growth will slow every year. Even with this estimation it is a market beating internal rate of return at 12% annual growth.

Our verdict

There’s a lot to like about this stock, from its low EV/EBITDA multiple to the increasing revenue. We expect this to continue for years and suspect they do have a competitive advantage or monopoly in their markets.

At a glance the company looks like it has a lot of debt, but with 1.9x Net debt to EDITDA, their debt is not that much. They are also paying it off though having recently announced the sale of some mast infrastructure and the IPO of a subsidiary in Malawi.

Overall we think we’re getting good value here with more upside, considering the growing earnings and even dividends.

Giles Capital confidence score: 8/10

Disclosure:

We have not purchased Airtel Africa, but are keen to do so soon.

Disclaimer:

This is not investment advice. Our content to be used for informational purposes only. It is important you do your own analysis before making any investment based on your own personal circumstances.

About:

Sign up to our free newsletter for more analysis & recommendations:

Stay invested and follow Giles Capital on Twitter at @GilesCapital.