Investing in quality: Topicus (TSXV:TOI) and Constellation Software (TSX:CSU)

Every month we'll be sharing a breakdown on our past or present investments. Previously we’ve discussed our investments in West Japan Railway Company in Japan and Bijou Brigitte in Germany. In this article we’ll look at two similar businesses: Topicus and Constellation Software.

What are Constellation Software and Topicus?

Constellation Software (CSU) and Topicus (TOI) are vertical market software (VMS) aggregators. Both acquire, manage and build VMS companies which provide software for other businesses that have specific needs. Topicus was formed as a partial spin-off of Constellation. To date, Constellation has bought and managed about 500 companies, while Topicus has bought and managed 85 companies. The simple table below gives a basic idea of how the two companies compare:

Constellation Software

Ever since its inception in Canada in 1995, Constellation Software (CSU) has been acquiring software companies. As a result it serves hundreds of thousands of businesses in a range of industries such as hospitality, healthcare, logistics and retail. CSU is made up of 6 distinct operating groups with each one managing many different business units. Business units are run autonomously and make product decisions, but have the resources and support of a 37 billion USD market cap company.

Topicus

Topicus (TOI), also known as Topicus.com, has a complicated origin. To over simplify, its beginnings start in 2013 when Total Specific Solutions (TSS) was sold to Constellation Software. This group would later spin back out of Constellation in 2020 and combine with another acquisition: a Netherlands-based VMS called Topicus.com. The merger of these companies is Topicus as we know it today, and like the parent company, it also trades on the Toronto stock exchange. We could look at Topicus as a mini European version of Constellation but with a much smaller market cap.

What makes these companies so great?

Focus on growth

Both CSU and TOI have a clear focus on acquiring, managing and building VMS businesses. Such businesses tend to have a stable and predictable cash flow and many growth opportunities. Opportunities can be found across the different businesses that CSU or TOI serve. The excess cash flow from the different business units can be used to make new acquisitions.

Decentralised but strategic

Decentralised management ensures the different business units make their own decisions regarding their customers and products. On the other hand capital is handled by higher levels of management, ensuring prudent and strategic capital allocation for CSU or TOI. Management from both these companies has a lot of experience on niche VMS businesses that are usually acquired for around $20 million USD or less and are able to use their experience to quickly reap payback and grow the business.

Scale, experience and expertise

In particular it is Topicus that benefits first from the merger of Topicus and TSS, but also from the experience of its parent company CSU. With the fragmented VMS market, TOI can start to make an impact by targeting and acquiring companies that fit its strategic aims. Knowledge across the different business units can be shared and leveraged providing additional value to customers and possible new streams of revenue or growth.

Stickiness

Because of the nature of VMS, niche industry and applications, the customers of these businesses rarely switch. There is little motivation to switch as the costs in doing so are high and contracts can be lengthy. Often there are very little in the way of other solutions for these businesses. The software and systems often used in government, education or in healthcare are examples of this. It’s precisely this stickiness of their products which makes a great moat for both CSU and TOI, who have lower customer churn, superior pricing power and higher returns.

Analysing both companies head to head

Let’s look at some of the financials to understand CSU and TOI more and see what stands out and which company fares better out of the two. Please note that TOI only has public financials for the last two years, while CSU has a decade and a half’s worth of financials.

What’s great

Profit

Gross profit margin for CSU is 88% vs TOI’s 90%. TOI is the slight winner here.

Net earnings as percentage of revenue for CSU is 10.3% while TOI is 12%, TOI is the slight winner here.

Over a decade EPS has almost tripled for CSU from 7 USD per share to 21 USD per share. TOI has a much lower EPS. CSU is the winner here, but the growth potential of TOI may be attractive.

Retained earnings growth over the last year for CSU is 16.6%, while TOI’s growth last year is an impressive 30%. TOI is the winner here.

Company

Cash and equivalents is good for both companies with cash equivalent to a year or two’s net profit. CSU has more cash relative to net income, but again TOI cash and equivalent’s growth looks attractive. TOI is the slight winner here.

Return on assets for both companies are similar at around 9.5%. This is good as capital is a barrier to entry for competitors and it seems consistent over time for CSU and between CSU and TOI. No real difference here.

Return on shareholders equity for CSU is 43%, while TOI is 23%. Both good but CSU is the clear winner here.

Goodwill is increasing for both companies, which is good to see but negligible when comparing them.

For property, plant, and equipment, both companies can easy pay off these costs with one year’s earnings which is good. The difference is negligible.

Debt

Interest expenses are low and both around 5%. TOI wins here by a tiny margin

CSU has 7 cents of short term debt for every dollar, while TOI has 58 cents per Euro. Both are decent but CSU is the clear winner here.

Both CSU and TOI have small amounts of long term debt and can pay it off with one years earnings but TOI seems a bit stronger here.

What’s okay

CSU has a higher debt to shareholders equity ratio than TOI, but both companies do not need large amounts to finance due to high cash flows. TOI is the winner here.

Depreciation of TOI is at 15%, while CSU is at 14%, so a slight win by CSU, but this is really minimal and almost insignificant for this type of business.

Regarding Capex, both use a large percentage of earnings but this is the nature of the acquisition business. CSU uses 85% of its revenue, while we don’t have a lot of data for TOI yet (they spent 151% on capex last year). CSU would be the winner here.

What isn't great:

Sales, General, Administrative costs are high for both companies. CSU spends 67% of its gross profit on it while TOI spends around 63%. TOI is the winner is here.

Revenue & PE ratio

Constellation Software

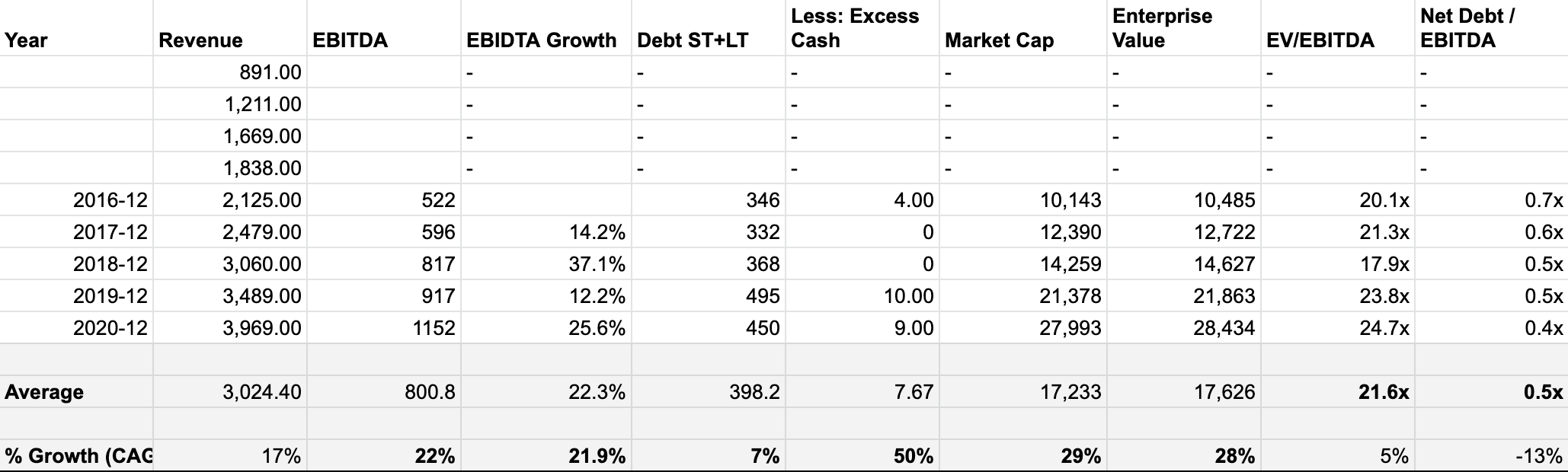

For CSU we can see that EDITDA has grown comfortable with a CAGR of 22%. We can see debt has been reduced over time. We also notice it is getting more expensive. Its PE ratio has gone up from 49 to 65 in the last few years. At today’s price its PE ratio would 87. Similarly, its average EV/EBITDA multiple is 21.6x, but at today’s price it would be 32x.

Topicus

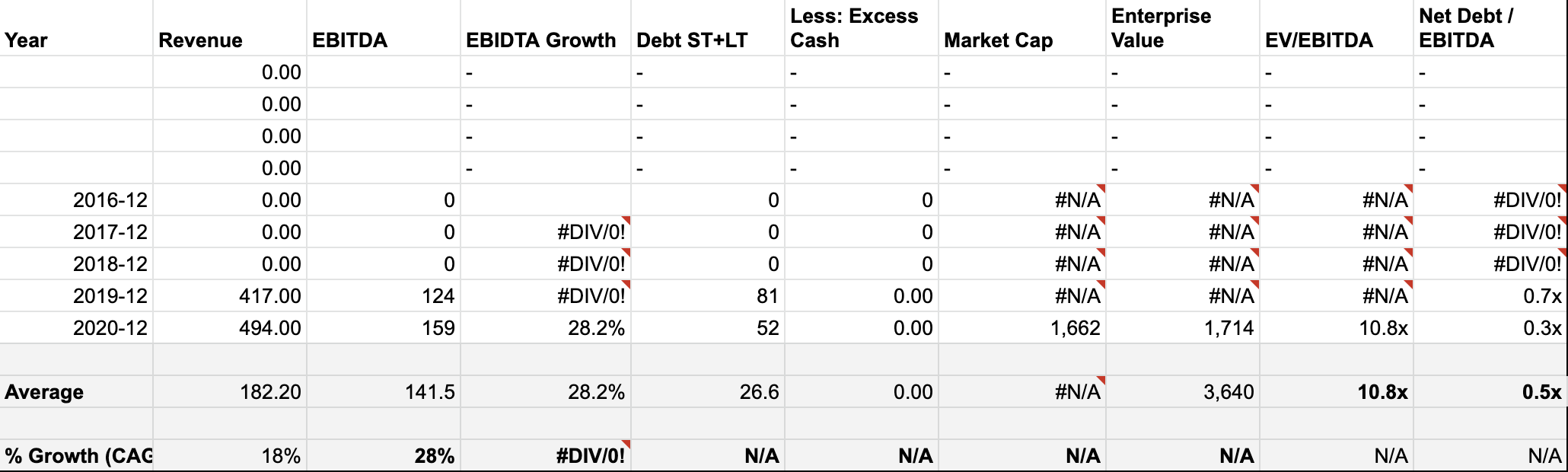

TOI has a much shorter history but it’s off to a good start with revenue growing 28% from 2019 to 2020. It has also impressively reduced its Net debt / EDITDA to only 0.3x. Last year it would have had a PE ratio of 26 and with today’s stock price 51. Similarly, last ear EV/EBITDA multiple is 10.8x, but at today’s price it would be 20.4x.

Cashflow

Constellation Software

Let’s take a look at the free cash flow. We can see quite a stable free cash flow being produced. Cash flow from operating activities has a CARG of 24.67% which is great. It also has yielded an average of 3.9% FCFE/yield every year, which is decent.

Topicus

What’s exciting about TOI is that we really see a similar picture to CSU. From 2019 to 2020 cash from operations grew 25.62%. Last years FCFE/yield was 6.0%. Again similar but slightly better figures than CSU.

Forecast

Constellation Software

For our EV multiple forecast, we can assume EBITDA will grow. Historically it has grew at around 22% per year. We then predict a declining growth, assumed by the fact there may be less companies to acquire and benefit from. This EV multiple forecast gives us a target share price of 7258 CAD:

For our FCFE forecast, we use a 2021 FCFE/share of 38.40 based on a 22.3% growth rate in line with our EBIDTA estimates. This gives us a target share price of 4156 CAD.

Averaging out these two forecasts gives us a share price of 5707 CAD by 2030.

Adding the FCFE/Shr back we model the future share price at 5870 CAD in 2030. This equates to an IRR of 22% which is market beating. We’re not using aggressive numbers so would predict this business to easily beat the market.

Topicus

For our EV multiple forecast, we can assume EBITDA will grow well. Last year it grew 28%, but we will use 25% and again predict a declining growth, assumed by less companies to acquire and turn around. This EV multiple forecast gives us a target share price of 382 CAD.

For our FCFE forecast, we use a FCFE/share of 3.40 based on an initial 25% growth rate in line with our EBIDTA estimates, which slows down over time. This gives us a target share price of 321 CAD.

Averaging out these two forecasts gives us a share price of 352 CAD by 2030.

Adding the FCFE/Shr back we model the future share price at 367 CAD in 2030. This equates to an impressive IRR of 36% which is by far beating the market. We are more careful about this forecast as it assumes the growth rate will be high but we do not have much historic data to base this on.

Summary

With our review of the financials and our forecast based on EBITDA and cash flow, TOI looks more attractive given it’s cheaper than CSU and has a higher expected IRR. However this does assume that TOI will follow in the footsteps of CSU.

As CSU owns 30.35% of TOI, it does have its best interests in TOI succeeding. Six members of the TOI board of directors are executives from CSU. If TOI can lean on this vast wealth of experience, it could avoid some crucial mistakes that could hinder its growth. We could already be seeing this in our analysis of the financials of both companies whereby TOI is better in 9 areas vs 4 that CSU are better in. But the real advantage here is that TOI is almost starting ahead and we’re able to catch it early, unlike CSU which has already compounded significantly over the last 15 years.

As an investor in either CSU and TOI, you will have your money managed in a tried and tested model by top class capital allocators. At 20x EDITDA today TOI may look expensive for some investors and but this is the kind of growth company we like. As Buffet says “It's far better to buy a wonderful company at a fair price, than a fair company at a wonderful price”. We believe it is good value for a tried and tested model which is hopefully more predictable than a vast number of other tech companies.

If TOI can achieve growth that comes close to half of CSU’s investors will be rewarded. With TOI being roughly 16% of the size of CSU, we believe it’s possible. Of course, following the same strategy may not always get the same results in a different part of the world. However, even though the history of TOI as a public company has been short, it is already off to a great start.

Giles Capital confidence score: 9/10

One of the highest scores we’ve had. Topicus is a high quality, punch card kind of business which we would like to hold over the longest period possible.

Further reading for much more detail on CSU and TOI:

Icaria Capital on Constellation Software

StockBros Research on Topicus.com

Interested to do your own analysis?

Check out our GCS tool that helps you pull in data so you can do your own analysis in Google Sheets. This is what we use to analyse companies financials statements.

Disclosure:

At the time of writing we do not hold a position in Constellation Software or Topicus, but interested to hold one in Topicus.

Disclaimer:

This is not investment advice. Our content to be used for informational purposes only. It is important you do your own analysis before making any investment based on your own personal circumstances.

About:

Sign up to our free newsletter for more analysis & recommendations:

Stay invested and follow Giles Capital on Twitter at @GilesCapital.

For Topicus' valuation, I see that you're using a fully diluted share count of 39 million. But it's 130 mil per their release: https://topicus.com/news-1/subordinate-voting-shares-of-topicuscom-inc-to-begin-trading-on-the-tsx-venture-exchange