A reader asks: Is TSMC a good investment?

A reader asks: Is TSMC a good investment?

Occasionally we'll answer reader's questions when it aligns with our possible portfolio interests. Today we'll look at the prospects of a Taiwanese Semiconductor company.

Taiwan Semiconductor Manufacturing Company (TPE: 2330 / NYSE: TSM)

Chips run everything from Amazon to our cars. In this world, TSMC is the world's largest contract chipmaker with 84% market share for the chips with the smallest, most efficient circuits and is a key supplier to Apple Inc. Its competitors, in our view, are mainly Samsung, with Intel in the rear view mirror. It's worth nothing Intel will be relying on TSMC in the future for some of its products. We won't go into much detail about chips here, but we suggest reading How TSMC has mastered the geopolitics of chipmaking for a start. In our view TSMC has a great lead in manufacturing chips, at least for the near future. We'll go into some of the financials to see whether it's a buy from our side.

What's great:

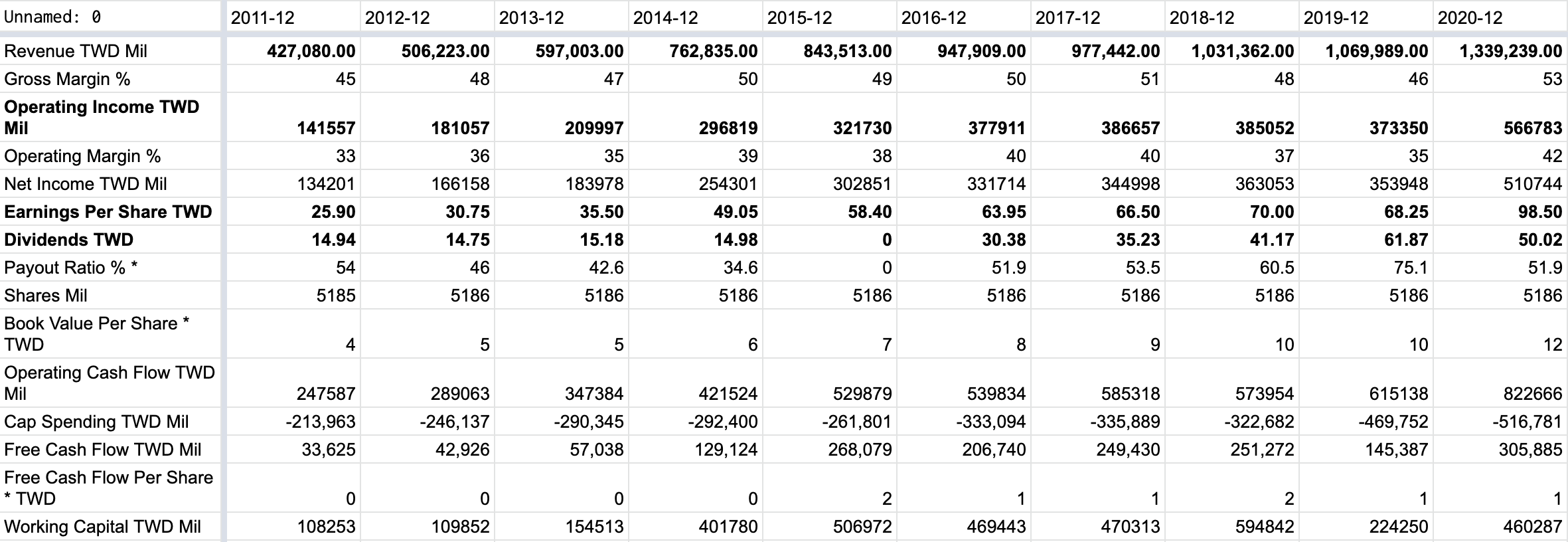

Profit

Decent top line revenue growth

Gross profit margin suggests a competitive advantage. It’s improving gradually over time

Net earnings are fantastic and perhaps slowly increasing

Earnings per share is improving over time

Efficiencies

Inventories are growing, inline with revenue growth

Retained earnings are shown

Return on assets is decent, but not too high that competitors could easily replicate

Property, plant, and equipment is easily payable with 3 years of their revenue

Number of outstanding shares have remained the same

Debt

Very little debt, little short time debt and therefore interest expense is extremely low

Good debt to shareholder equity ratio

What's OK:

Combined spending on Selling, General, Administrative and R&D is over 60% of gross profit. This is high, but in other years it has been under control. This is a competitive field so it is acceptable, but not great.

What's not great:

Depreciation looks high, although stable

Goodwill is decreasing, which suggests no acquisitions of companies or at least not great ones

High spend on Capex

Analysis & price targets

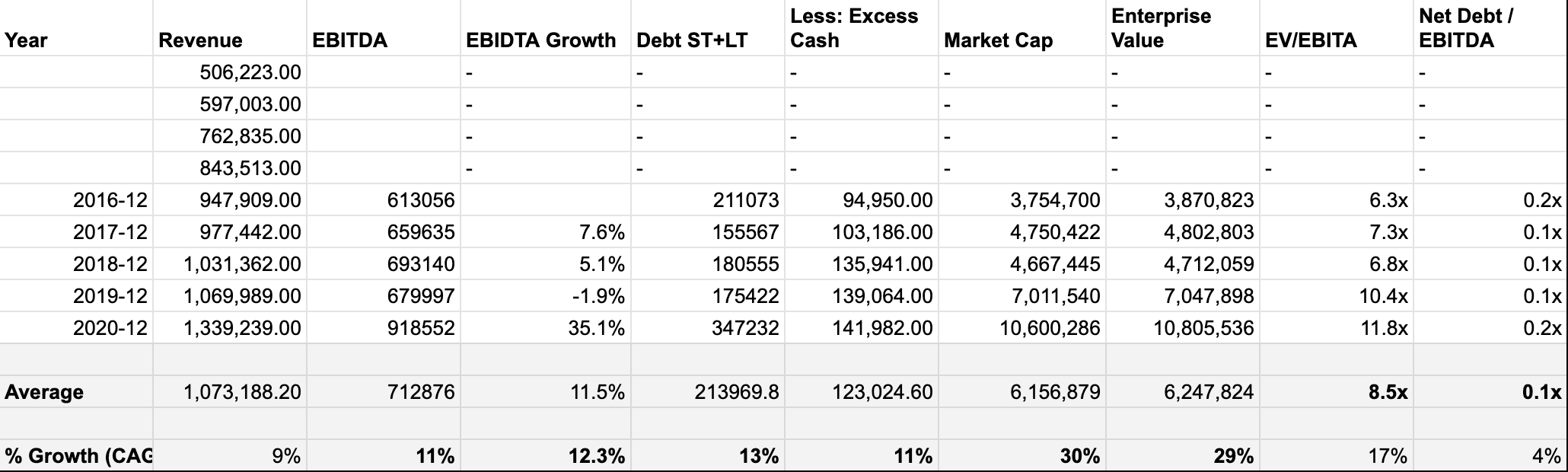

Here we can clearly see a good growth in top line revenue over time. EBITDA has also grown and is expected to grow further. Although the company has been cheaper in the past, the EV/EBIDA ratio is not bad and less than average (compared with the S&P500) which suggests its not too expensive, but not undervalued. It is worth noting there are many, much more expensive tech companies though.

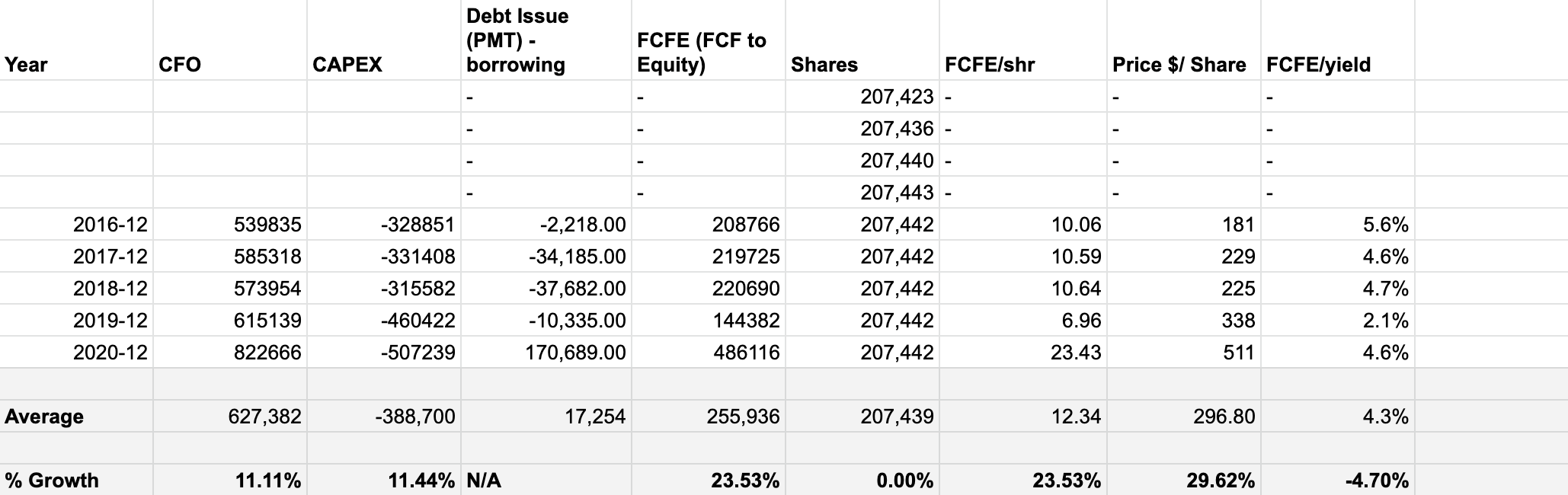

We can see free cash flow has also grown in line with revenue and EBITDA. This is great to see and we would expect this to continue.

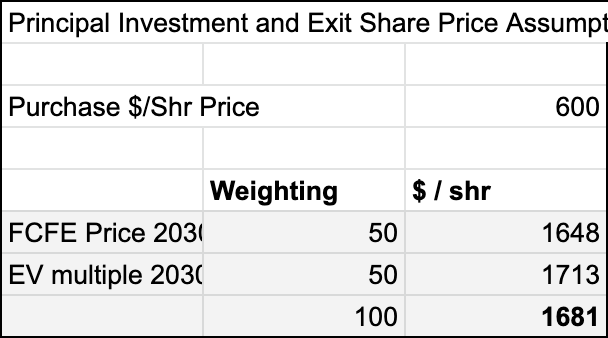

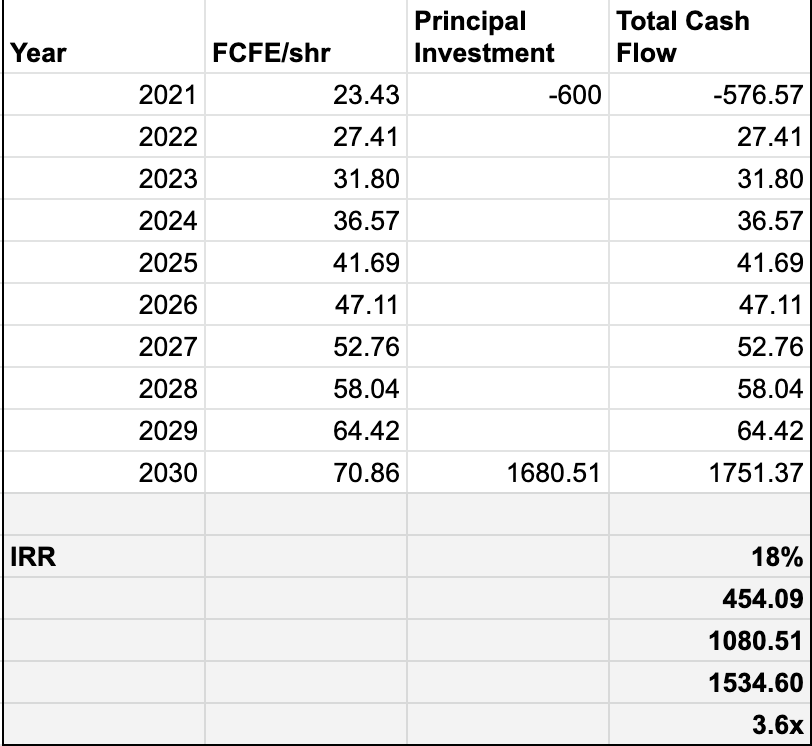

Averaging out a free cash flow model and EV multiple model, we get a 2030 price target of 1681 NTD, compared with a current price of 600 NTD.

Overtime this gives an IRR of 18% which is definitely a market beating return and we’d expect this company to beat the average performance of the S&P500.

Our verdict

While it doesn't scream undervalued, TSMC is a solid company when looking at the financial statements. It indicates it has a sustainable competitive advantage. There are competitors, but in the short run we think TSMC will be the winner here. Particularly as we expect the demand for the best chips, which may be used in smart appliances and EVs, to continue to grow. It is worth considering it might take years before Intel can attempt to catch up which is why it looks like its better value.

TSMC is not cheap historically, so any interested investors should not be looking to sell it anytime soon. Over a longer period of time, this stock has the potential to beat the market. We think there might be better stocks, but would not mind holding this over the long term, or buying if the stock price gets lower.

Disclosure:

We do not currently own TSMC, but may open a position in it in the near future.

Disclaimer:

This is not investment advice. Our content to be used for informational purposes only. It is important you do your own analysis before making any investment based on your own personal circumstances.

About:

Sign up to our free newsletter for more analysis & recommendations:

Stay invested and follow Giles Capital on Twitter at @GilesCapital